I am writing this post for one reason –

To debunk a terrible, bullsh** study which concludes that:

“The later you retire, the earlier you die.”

Sounds…intriguing?!

Retire early = live longer?!

Retire later = die sooner?!

It pains me that a bunch of suckers in my line of business (creating educational personal finance content) either don’t have the common sense to really think about these results, or are too cynical to care that they’re re-posting bullsh**. See below:

I know I’m not the only one thinking, “Jesus, where’s the common sense?”

[Author’s note – thankfully, some fantastic retirement researchers were inspired by my LinkedIn post about this topic and they decided to write a professional / academic take down of this bunky study. Their article is here.]

Forgive me for my attitude.

But this study is making the rounds among thousands and thousands of retirees and soon-to-be retirees, and it’s clear that many people are falling for it.

This “study” is totally false. So please – if you ever see this study shared online, simply share this article in response to help those would-be suckers.

Let’s get to de-bunking.

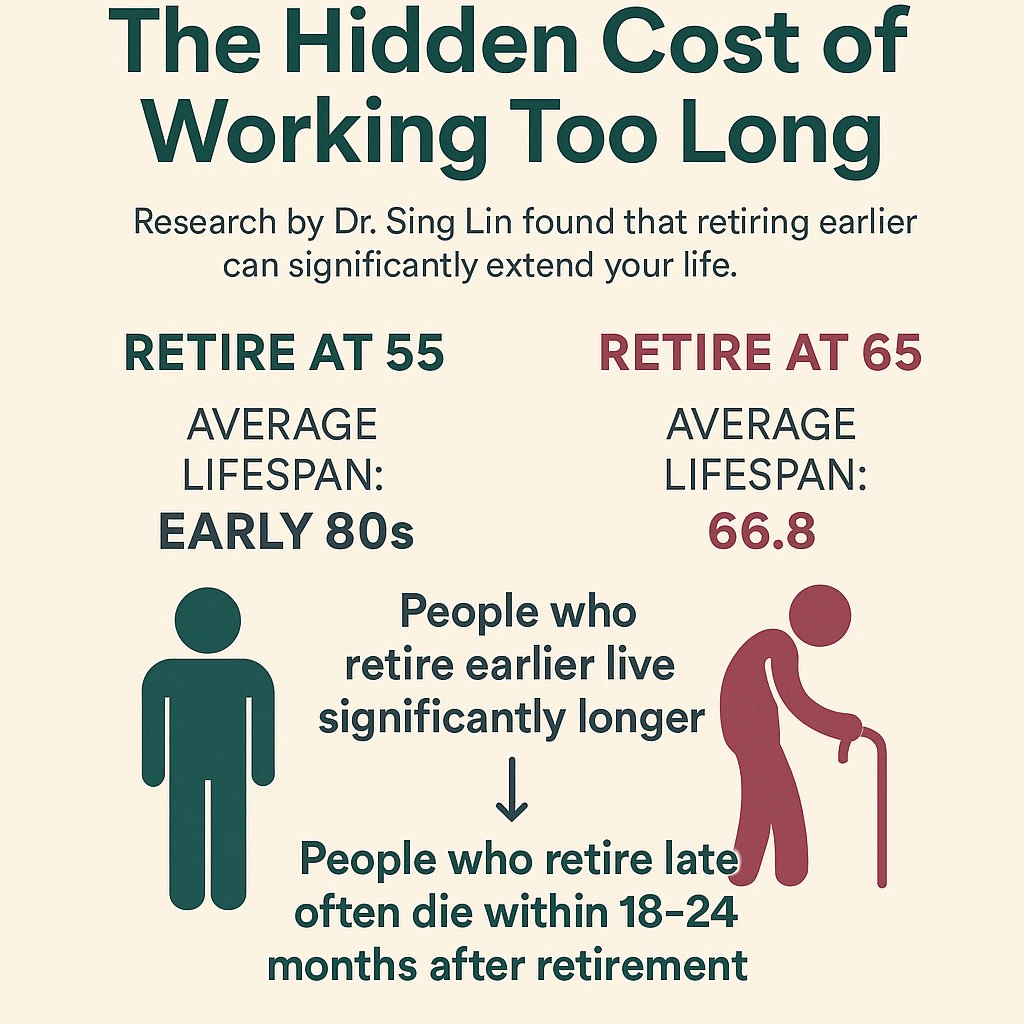

Retire Early, Live Longer. Retire Later, Die Sooner.

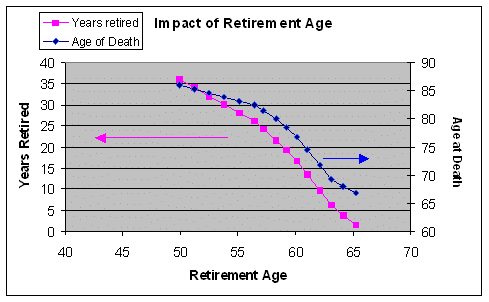

It’s pretty simple. This “study” suggests that the average early 50s retiree will live to their mid-80s, while the average mid-60s retiree will live less than 5 years more.

Roughly, for every year you retire earlier, you’ll live at least one year longer.

Retire at 60? You’ll live to 77.

Retire at 55? You’ll live to 83.

What a sobering stat, if true.

But…

The Common Sense Filter

First, let’s use common sense.

Of the many smoking guns here, I’ll just skip to the biggest one:

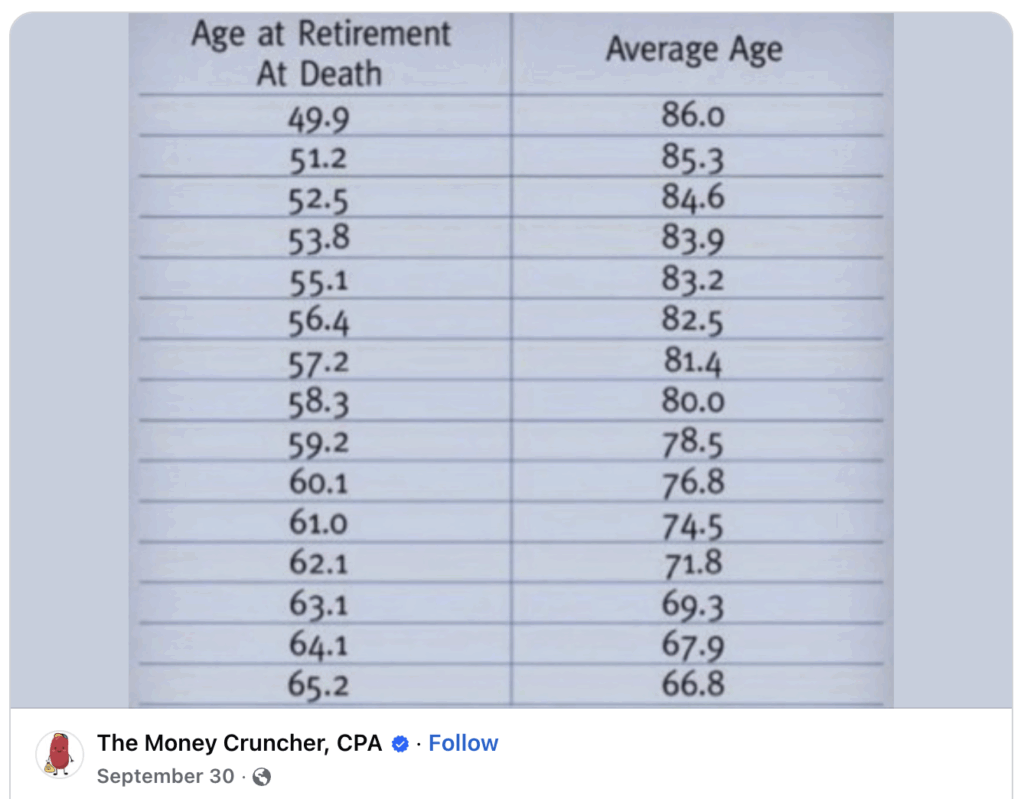

The average person who retires at age 65 will die by age 67?!

Does that pass the sniff test in any way?

Let’s keep going to ages 66, 67, 68, 69, etc. (which conveniently aren’t in this study).

Does the average person who retires at 68…just immediately die?

Do they hop in a time machine to die at 67? Whoa, it’s 2024 again..aaaannnd I’m dead.

Did the people who created this study not consider these obvious questions?

The Lived Experience Filter

We’ve all lived a long time and met a lot of people.

Surely a result as stark as this would mesh with our lived experience in the world, at least to some degree.

The Causal Filter

Let’s ask what if.

What if this study is actually correct? We ought to then wonder, “what would the causal factor be that’s leading to this result?”

Why does each year of earlier retirement actually lead to longer life?

The most frequent answer seems to be, “Work is so stressful. You leave work, no more stress, you live way longer.”

But if that was true, surely people would be dying AT WORK!!! Why aren’t more people dying at their desks from all the stress?

If work is that stressful, then the act of leaving work, at any age, ought to fundamentally decrease one’s mortality, not increase it.

The “Why Haven’t I Heard of This?” Filter

We all know that smoking increases mortality. We know that.

So does heroin and being 200 pounds overweight.

If you’re smoking, shooting heroin, and 200 pounds overweight, you better quit your job right away.

We’ve all heard of the real factors that have the biggest impacts on our mortality. For example, the CDC states that smokers’ life expectancies are at least 10 years shorter than non-smokers.

10 years of life expectancy is a huge deal. That’s why you’ve heard of how bad smoking is.

So – why aren’t more legitimate people shouting about this “retirement risk factor” from the rooftops?

The Distribution Filter

The American Academy of Actuaries (aka the foremost experts in longevity) includes 4 factors when helping retirees estimate their potential lifespan. Those four factors are:

- Current Age

- Gender

- Smoking Status

- General Health

The age at which you retire does not affect their estimates or probabilities of when you’ll live.

But even then, we need to consider the distribution! Meaning – should we think of longevity as one specific “average age of death?” Or as a spectrum of ages and probabilities?

It’s a spectrum. Not a specific age.

The “Shitty Decimal” Filter

Personal pet peeve, but it has merit, too:

Why are there tenths of years in the “Age at Retirement” column? Why aren’t they simply, whole numbers?

The independent variable in a study like this should be straightforward to express, so the results are easy to understand. We don’t need, nor want, to understand tenths of a year there.

The study looked at retirees of age 55.1, 56.4, and 58.3.

It should be 55, 56, 57…etc.

The fact that it’s not that way? It’s just poorly done. And that raises suspicion.

Where Did This “Result” Come From?

Let’s pivot. Where did this bad study come from in the first place?

I had to do a little Internet rabbit-hole digging. Here’s what I’ve got:

In 2002, a Chinese/Taiwanese PhD named Sing Lin (who I couldn’t verify actually exists) “published” this “paper” where derives inspiration from Japanese physicist named Leo Esaki (who does exist, and won a Nobel Prize in Physics).

Dr. Esaki inspired this research by observing that for many people, their most creative years occur in the 20s and 30s, and that most people fall off precipitously in older age.

In a beautiful ironic twist, Dr. Esaki was still working as recently as 2021, at the age of 96. Clearly, later retirement has harmed his longevity.

The author, Sing Lin, then pivots to another PhD, Ephrem Cheng (who I couldn’t verify actually exists), who is cited in the paper for providing the statistical data after analyzing Boeing Corporation’s pension data. Supposedly, other large corporations (Lockheed, Ford, IBM) had similar data sets.

These data sets all indicated that later retirees died sooner.

Compelling?

Well, it was compelling until Boeing responded in 2004 to say, “You know that weird ‘study’ that’s going around and supposedly uses our pension data? Well, our actual pension actuary experts took a look and the whole thing is baloney.”

Here’s the memo from Boeing.

The study is simply false.

And What Does Research Actually Say?

As for real research, I’m officially out over my skis here. I don’t know statistics, actuarial science, or longevity research.

But I can read English!

Here’s the summary from a peer-reviewed study in the Journal of Epidemiology and Community Health. The study has the catchy name: “Association of retirement age with mortality: a population-based longitudinal study among older adults in the USA“

Here’s the part I do understand:

“Results: …a 1-year older age at retirement was associated with an 11% lower risk of all-cause mortality…”

In other words: older age of retirement, LOWER risk of death.

“Conclusions: Early retirement may be a risk factor for mortality and prolonged working life may provide survival benefits among US adults.”

Well. That’s the opposite of our apocryphal study.

Retire, Don’t Die

Let’s bury the hatchet in this fake study.

Retiring later isn’t a death sentence, and retiring early isn’t the holy grail.

This guy below is still working at age 700+!!!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Good article! I have seen these posts all over my Facebook feed as well.

It is a sad new online trend, post incorrect things and stir people up, get engagement, make a little money.

It is not just fake studies, there are numerous meme posts that are slightly to massively incorrect. One you may have seen would be “if you were born in 1985, you would be 30 this year” overtop a picture of a famous 80s movie.

You feel a little rage at this bad math and leave a comment about the error……and that right there, is your introduction to “advanced click bait 201: enrage users with incorrect information”.

Cheers Will. You’re right. I can only come to two conclusions… they “either don’t have the common sense to really think about these results, or are too cynical to care that they’re re-posting bullsh**.” If it’s the second one – pretty sad!

Well done. I too saw that study floating around and thought this is such nonsense. Took the time to reach out to Warren and he corroborated what he learned from Charlie. Work longer. Stay married. Live longer. Ditch the FIRE community.

Hi Jesse, I heard on another finance podcast that the “retire earlier die sooner” phenomenon is largely attributed to people who are forced to retire early, and lose meaning and purpose and therefore health, and this population is much much larger than the “choose to retire early” cohort, so the data is skewed as a result. The podcast said that finally researchers had separated the FIRE folks from this larger “forced to retire early” population, and indeed choosing to retire early does increase lifespan. But it can’t control for things like health and diet, etc, and my hypothesis is that FIRE folks are more dialed in to these healthier lifestyle choices. I don’t remember the podcast episode but I’m sure if you dig into this a bit more you’ll quickly find that episode and the recent study they referenced. Thanks for the great content!

Thanks for those thoughts, Raj.

If those podcasters have the data to back it up, I’m all ears!

Here’s an interesting wrinkle: somewhat inspired by my recent work, two very well-respected retirement researchers just penned a new article today. See it here:

https://thinkadvisor.com/2025/12/11/is-delayed-retirement-bad-for-your-health

I am not sure why the “choose to retire early” cohort would have any longer or shorter lifespan than the “choose to retire at a more normal age” cohort. I don’t understand how any significant causal factor could be there.

I do, however, understand how the “forced to retire early due to health” cohort would have significantly less lifespan than any other. We are literally selecting for bad health in that cohort.

Good food for thought!

25 years ago, a 55 year old co-worker went around the office and slapped a copy of the “Boeing data” plot on everybody’s desk. “This is why I am retiring today!” he told everyone.

As a 30yo at the time, I had no reason to disbelieve the data presented, it seemed legitimate when observed in a vacuum.

I still have the plot in a folder somewhere….

Yikes! Some urban legends not only linger, but grow in magnitude over time!