If you missed Part 1, check it out here.

Misconception #4: Savers, early-retirees, individuals who write this blog…they’re all penny-pinching hoarder scrooges who sacrifice quality of life for a small bump in their bank accounts.

Corrected #4: I can I can only speak for myself, but I love my quality of life. I think I do the same things as just about everyone else, but I just try to adjust the financial knob when I can.

I host parties, but spend $15 on pizza ingredients rather than $40 on a couple of delivery pies. I volunteer coach at my alma mater, which grants me the fulfilling role of teaching and interacting with bright young athletes, while simultaneously getting free access to the excellent university gymnasium. I read constantly online and from the library rather than purchasing books or a magazine subscription. I go to the mall, but I usually stop at Goodwill or Salvation Army first. I feel the same impulse that leads to “impulse purchases,” but I try to quell it rather than letting it take control (although I will write one day about my biggest financial impulse failure…not a fun story).

Sure, some folks in the money-saving blogosphere don’t own cars, gauge their groceries on a calories-per-dollar basis, or wash their clothes by hand in the local fresh-water stream. To you and me, maybe those situations would hurt our quality of life. And I can’t speak for those folks…maybe they actually hate rice, but 12-cents-per-1000-calorie ratio is just too sweet to pass! All I can say is…to each their own, and I’m digging this homemade pizza.

Misconception #5: I don’t know a lot about personal finance, so this blog is gospel. I need to follow all the opinions I read here. I need to save more, spend less, sell my car, eat more rice…

Corrected #5: Saving more is generally good. Spending less is generally good. There are times when spending money is great, like if your spending it on a solid investment. Sometimes, putting money in your 401(k) is bad, perhaps because your emergency fund is almost at zero and your 25-year furnace just turned 30. Rules have exceptions, but they are generally good to follow.

Your situation is different than mine. It’s also different from the kid who just graduated college, different from the woman who is about to retire, or from the couple who just had their 4th kid. Everyone is different. You need to evaluate your own timelines, your own ranking of what’s important, what will improve your quality of life and quantity of life.

We might not be in the same position. Some people have a trust fund that sets them up for life, while others have had to completely fend for themselves. Some things I write won’t apply to you, won’t work you, or might straight up be bad opinions for your specific situation. If unsure, feel free to reach out! I’m just an engineer with an interest in personal finance, but I’m happy to lend you my opinions.

Misconception #6: You’re throwing away money by renting! Or…Your mortgage payments are all interest, no principal; that housing purchase was so stupid!

Corrected #6: I don’t mind standing on the shoulders of giants here. Other folks have already tackled this debate, and done so using easy-to-use calculators online. In short, a lot of factors go into this argument.

- What’s your rent?

- What would your mortgage payment be? What’s the interest rate? The term length?

- How long will you live in your current location?

- What are the taxes like?

- What’s the renter’s insurance like? The potential homeowner’s insurance?

- Is your rent increasing year over year? Do you expect your home value to increase year over year?

It’s complicated! Way too complicated for an average Joe (or even a really Interested Joe) to figure out on his own. So, I highly recommend you stand on the shoulders of giants, too. I really like this calculator from NerdWallet. It’s easy to use and gives nice visual results. I used it before I bought my house, and was quite relieved when my result was, “If you stay in your home for at least 1 year, buying is cheaper than renting.”

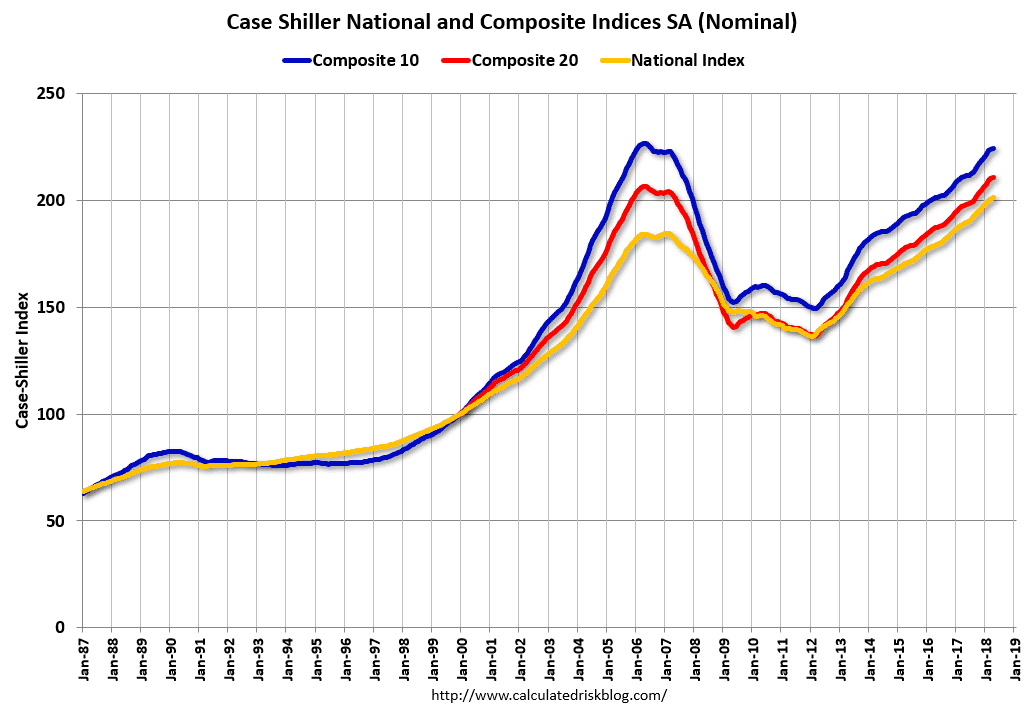

Then again, some folks will tell you that housing prices are getting out of control again, just like they did before the crash of 2008. And it’s hard to argue against that idea. The “Shiller Index” is a metric that’s used to compare housing prices over time. Obviously, we’d expect houses to be cheaper in 1950 than they are today. But when we compare that 1950 price against the economic conditions of 1950, and the today house against the economic conditions of today, we get an apples-to-apples comparison. It normalizes these different prices to make comparison easy, and an index score of 100 is average.

When we observe the Shiller Index since 1990, we see that the prices right before the 2008 recession—when we know that housing was in a giant bubble—were very high. Over 180! The recession started to reduce those prices, but then… since the early 2010’s the Shiller Index has continually increased to above pre-2008 levels. To many folks, this is concerning, and a reason to hold off on any housing purchasing until—perhaps—our current peak ends in a similar manner to 2008.

What other misconceptions have you come across in your financial travels? As always, thanks for reading.

Nice Job, JC! ps) your intro post uses “the Best Interest” but elsewhere it reads “The Best Interest”….do you want a capital ‘T’ ?

It looks like the housing shiller index has nearly doubled since you posted this. Should I be concerned as a homeowner?

-Not a market timer