You’re seeing Silicon Valley Bank (SVB) in the news. People are comparing it to the Great Financial Crisis in 2008. What’s going on?

Let’s talk about Silicon Valley Bank in simple terms.

I’m writing this ~2pm EST on Sunday March 12. I will update this article as more information comes out this week.

If you’re rather listen to this content, check it out in Episode 50 of Personal Finance for Long-Term Investors (formerly The Best Interest Podcast):

How Do Banks Work?

First simple question: how do banks work?

Banks have assets and liabilities. Most of you are familiar with both ideas (even if you don’t realize it).

The liabilities are deposits, just like the money you deposit in a savings account. You’re a depositor. Since the bank owes you that money back, plus interest, it’s a liability on the bank’s balance sheet.

Assets come in two forms: loans and securities.

Banks give personal loans, business loans, mortgage loans, etc. They charge a higher rate on the loan borrowers (say, 6%) than they pay to their depositors (say, 1%). That difference (in this case, 5%) is called the net interest margin (NIM), and is the main way banks make money.

Banks can also choose to buy securities using depositors’ money. Most commonly, securities take the form of short-term, high-quality bonds, like 3-month or 6-month U.S treasury bills.

Most banks perform better when interest rates rise. They are able to increase their NIM, making more money off their loans, and generating more profit. The more a bank relies on loans, the better it does when interest rates rise.

But if a bank relies heavily on securities, the opposite is true. Rising interest rates hurt bond prices and hurt the bank’s bond portfolio. This is a simple fact of bonds. Why own an old bond yielding 3% when you can buy a new bond yielding 4%? The old bond loses lustre, and loses value.

The more a bank relies on securities, the worse the bank will do when rates rise. This is especially true if the bonds have longer durations (e.g. a 5-year U.S. treasury has a longer duration than a 3-month Treasury).

What About Silicon Valley Bank?

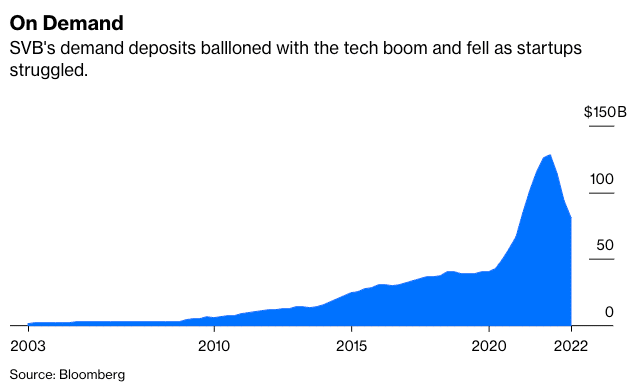

SVB specializes in helping tech companies. The bank has grown rapidly in recent years because of that focus.

Many tech companies raise large sums of cash (through venture capital, private equity, or by going public), then deposit that cash at SVB.

Being cash-heavy, those tech companies don’t need loans. Hence, SVB had lots of excess deposits. What’s a bank to do with the extra money? Buy securities. Unlike most banks which are loan-heavy, SVB is/was uniquely securities-heavy.

The First Cracks in Silicon Valley Bank…

As interest rates rose over the past year, “easy money” dried up. Many of SVB’s depositors (tech companies) stopped making new deposits. Less venture capital, less private equity, and fewer initial public offerings.

Deposits were only leaving the bank. In fact, many early-stage tech companies hemorrhage cash by their very nature.

Over the past ~10 years, SVB’s concentration in tech companies has been helpful. It meant tons of new deposits were flowing into the bank.

But concentration is a double-edged sword. Over the past year, those deposits have only been leaving the bank.

Remember: most of those deposits are not sitting as cash in a safe. Instead, those deposits have been:

- Used as loans to other bank customers

- Used to buy securities

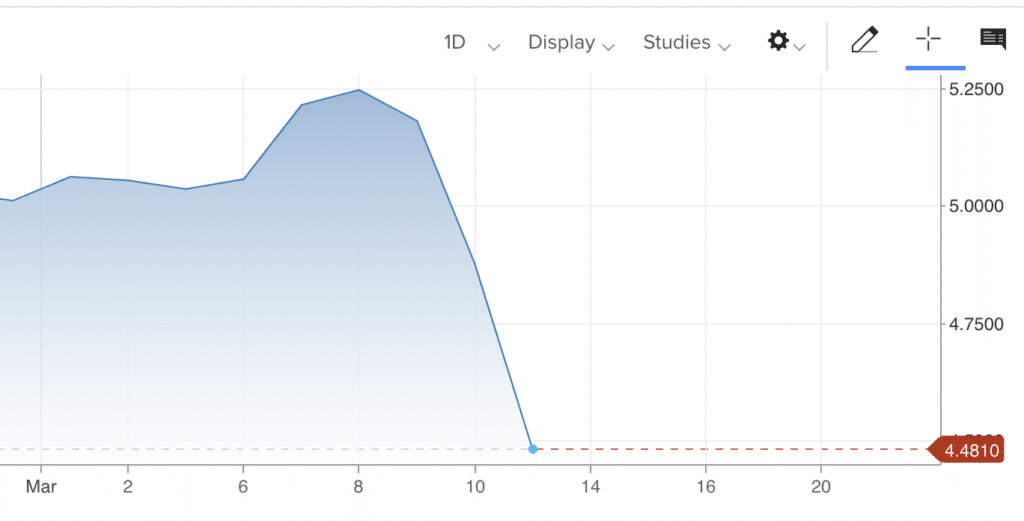

If too many depositors need too much money back from the bank, the bank needs drastic action to raise cash. SVB needed to do that last week: raise cash. SVB sold ~$21 billion of its bond portfolio on Wednesday. Interest rates spikes early last week after Federal Reserve chairman Jay Powell’s press conference. That spike hurt SVB’s bond portfolio, lowering the value of the bonds they held.

So SVB’s $21 billion bond sale came at an estimated $1.8 billion loss (e.g. they purchased the bonds for ~$23 billion). For SVB, that loss is more than a full year of profits. For a bank (generally a “safe” business model), that is a huge loss.

And it begs a scary question: how much trouble must SVB be in to do something so drastic?

In another attempt to raise money, SVB tried selling more shares of its stock (an amount equivalent to ~30% of the bank’s total value, diluting current shareholders’ ownership by 30%). This caused SVB’s stock price to crash even further, and the cash raise ultimately failed. It begs a similar question as above:

Why would SVB sell off shares of stock now (at $200 per share) instead of last year ($600 – $700 per share)?

A Run on the Bank

SVB’s weakness caused a tidal wave of $42 billion in attempted withdrawals on Thursday, March 9 alone. As of close-of-business on March 9, SVB had a negative cash balance of $958 million.

Perhaps you’ve seen this scene in It’s a Wonderful Life? It’s a great learning lesson. Give it a watch.

When depositors lose confidence in a bank, they want their money back. This compounds the bank’s problems.

And it’s exactly what happened to SVB this week.

In the Great Depression, many banks completely failed, leaving their depositors hung out to dry. That’s when the Federal government decided to pass the Banking Act of 1933 which created the Federal Deposit Insurance Corporation, or FDIC. The FDIC insures bank deposits up to $250,000. You, me, every American with money at a bank is insured up to $250,000.

The FDIC stepped in on Friday March 10 and took over Silicon Valley Bank. Depositors at SVB are safe…but only up to $250,000! That’s scary for some people, who might have had millions in their accounts at the banks. What happens to their money?!

Will Silicon Valley Bank Be Rescued?

There are two main ways the SVB could be “bailed out.”

The first is that the Federal government steps in above and beyond the FDIC’s $250,000 limit. This is what happened in the Great Financial Crisis, when $200 billion was given and/or loaned to banks to ensure they stayed alive.

As of 2pm EST Sunday March 12, Treasury Secretary Janet Yellen said the Federal government would not pursue this course of action. This is a very delicate topic. We’ll revisit it below.

UPDATE, 6:30PM EST Sunday March 12: The FDIC and Federal Reserve are fully protecting all depositors, who “will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.”

The second possibility is that another private institution agrees to buy SVB, likely at a steeply discounted price. This is what Warren Buffett did during the Great Financial Crisis, injecting cash into Goldman Sachs and Bank of America in exchange for a large share of those two banks.

But famously, Buffett said no to Lehman Brothers and AIG. Lehman failed completely. AIG got U.S. bailout money.

The important point is that SVB depositors – and by proxy, American depositors as a whole – are made to feel confident they’ll receive 100% of their deposits back.

To Bail Out or Not Bail Out?

Should the Federal government bail out SVB by giving it money to make its depositors whole? In my opinion, there’s no good answer.

If the government does bail out SVB, it reinforces the following precedent:

Hey, American banks. Do whatever the hell you want. Be irresponsible. Cut corners. Squeeze every profit out of your customers. Over-concentrate your business. If you screw up, you’ll pay no consequences.

This is called moral hazard. It’s the “lack of an incentive to protect against risk.”

If the government does not bail out SVB, it sends the following message:

Attention all banks, all depositors, all loaners, and all investors in banks stocks: you are on much thinner ice than you previously assumed.

This outcome could cause a “crisis of confidence,” where perfectly healthy banks are called into question.

Fear is extraordinarily contagious.

Warren Buffett

“How do I know my bank isn’t the next SVB? Maybe I should go pull out all my money now…”

Perhaps a second run on a questionable bank occurs. Then a third and a fourth, but on reasonably safe banks…then boom, boom, boom it’s happening all over the country.

This would be a “financial contagion,” an outcome far worse than a single bank failure. Avoiding financial contagion is a must, and is 100% why the Federal government stepped in during 2008.

Are Other Banks in Trouble?

As noted earlier, Silicon Valley Bank is unique in a few ways. Those unique features directly led to its failure. Most other banks are, unlike SVB, actually stronger today than they were one year ago.

Remember: most banks are loan-heavy. It’s easier to profit from loans when interest rates rise. Those banks are stronger now than any time in the past decade.

Unlike SVB’s concentration in tech company customers, most banks have a diverse portfolio of customers. They are not exposed to the same “concentration risk” as SVB.

On merits alone, the U.S. banking system is not in trouble.

The only fear, literally, is fear itself. Any sort of financial contagion won’t be based on banking fundamentals, but instead would be caused by collective depositors’ fear. Our leaders have to ensure that won’t happen.

I’m writing this ~2pm EST on Sunday March 12. I will update this article as more information comes out this week.

UPDATE: Tuesday March 14, 9:00 AM…

What About Signature Bank?

Another big bank failed over the March 12 weeked – Signature Bank of New York. Signature is the 3rd largest bank failure of all time (with Silicon Valley Bank coming in at #2).

When SVB got weak last week, Signature Bank fell under the microscope due to its connections to the crypto industry (e.g. common tech-based connections with SBV).

Depositors rushed to withdraw funds (roughly $10 billion) from Signature Bank on Friday March 9, and the FDIC swooped in to take over the bank on Sunday March 11.

Was this FDIC takeover merited? Depends on who you ask.

Coincidentally, one of Signature Bank’s directors is former Congressman Barney Frank, one of the main authors of the famous Dodd-Frank banking laws that were written after the 2008 Great Financial Crisis.

According to Frank, the FDIC did not have a legitimate reason to step in at Signature Bank. Instead, they did so purely for optics. That is, to give the appearance that they’re squashing any hint of financial contagion.

“I think part of what happened was that regulators wanted to send a very strong anti-crypto message,” Frank said. “We became the poster boy because there was no insolvency based on the fundamentals.”

…

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Excellent, clean and concise article! Thank you. People need to realize this isn’t endemic, HOWEVER (all caps) it does beg to reason the unsound nature of Gramm-Leach-Bliley, repealing that and reinstating Glass-Steagal. I realize this may be a broader subject, but harkening back to 2008-09 makes this relevant. Memories being short, and the love for easy money running deep, I think we will see a repeat of the financial crash again if we don’t bring back stringent banking regulations.

Old man out,

Thanks!

Joe Bob – thanks for the kind words!

I agree with you. Ultimately, this comes down to SVB seeking too much risk/reward in its security portfolio. Greed and/or stupidity.

If this is what lack of regulation leads to, then more regulation is needed.

At first I thought this was caused by SVB investing in too risky of securities but they were in bonds and T-bills. And those had their worst since uh maybe ever. They weren’t taking on too much risk. They had a ton of deposits due to the nature of the industry they played in and invested those deposits conservatively. Their mistake was focusing too much on one industry. They weren’t passing around toxic assets like the banks did in ’08 though crypto bros might call T-bills toxic!

I’m all for reinstating Glass-Steagal types of regulation though. Make Banks Boring Again!

Hey Rayfes – thanks a ton for reading and writing in. We’ll learn more as details come to light, but my understanding is SVB’s bond portfolio contained more risk and more duration than typical banks’ portfolios.

If all SVB held were 3-month treasury bonds, we wouldn’t be here.

Instead, they held mortgage-backed securities and 10-year bonds. More duration = more interest rate sensitivity.

Agreed that boring banks are better! 🙂