Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

In Morgan Housel’s book Same as Ever: A Guide to What Never Changes, Housel recommends that people,

“Plan like a pessimist and dream like an optimist.”

But pessimism and optimism are opposites, and feel like they shouldn’t coexist. Most people struggle with holding opposing views at the same time. But Housel argues this is an important exception:

“They seem like conflicting mindsets, so it’s more common for people to prefer one or the other. But knowing how to balance the two has always been, and always will be, one of life’s most important skills.“

Housel uses illustrative examples to further bolster his point, but I want to apply his recommendation to retirement planning, because it’s a perfect idea.

“Plan Like a Pessimist…”

How much should you have in cash or (more likely) low-risk bonds as you start retirement?

I think about matching my future liabilities with specific assets. And I do my best to ensure those assets don’t lose value between now and the liability date.

If the liability date is tomorrow, I can’t afford to take any risk. I need to invest in something like a Treasury bond.

But I expect that eventually, my liability date is far enough in the future that I can take investment risk and still feel like the money will be there when I need it.

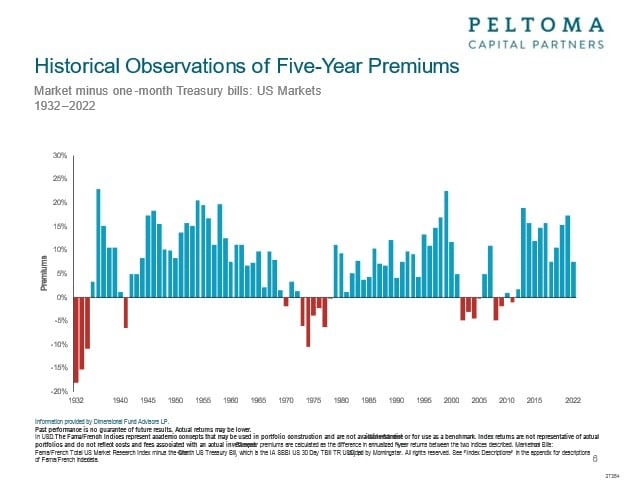

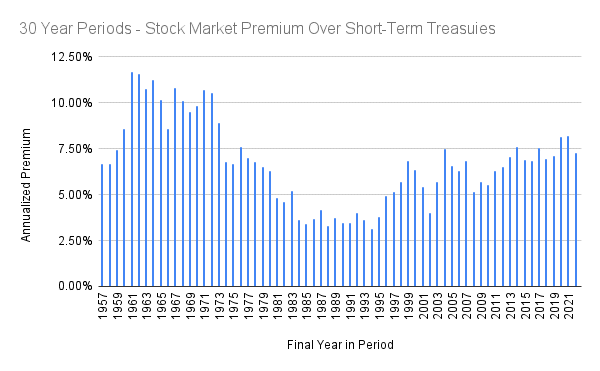

So I start by looking at charts like this one…

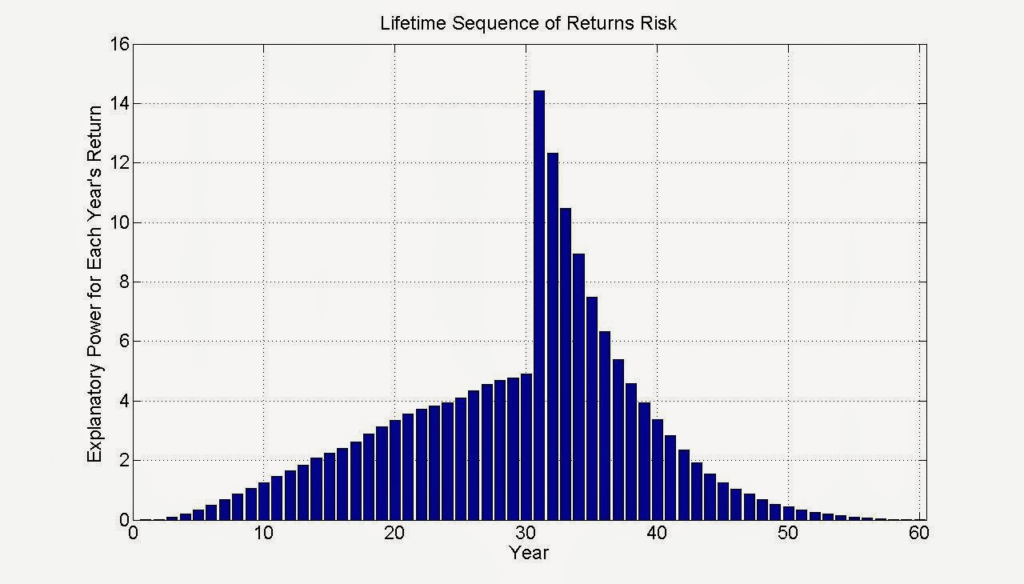

…and I think that five years is usually enough time for stocks to outperform bonds. Then I look at charts like this one…

…and think that six years is usually enough time for the sequence of returns risk to decrease to pre-retirement levels.

Simple conclusion: perhaps I want to build six years of safe Treasury bonds into the start of my retirement plan.

I realize that cash and bonds usually underperform stocks. The math there is straightforward. But we also know that stocks have had 5-year periods of negative performance. And, being a pessimist, I don’t want to knowingly underfund my future liabilities. Every timeline is unique, and we don’t know which timeline we’ll live through over the next 5+ years. Will we get a terrible run of stock market returns? My crystal ball is as foggy as yours.

So I’m planning like a pessimist. For the next 5-6 years if not longer, I can see a scenario where Treasury bonds outperform stocks, and I’d want my next ~6 years of spending to be allocated to safe Treasuries.

I want that margin of safety in my retirement plans, and I am willing to accept “lower returns on average” in exchange for that margin of safety. Ben Graham (Warren Buffett’s most significant mentor) once quipped:

“The purpose of the margin of safety is to render the forecast unnecessary.”

If I build a sufficient margin of safety into a retirement plan, it “renders the forecast unnecessary.” I don’t need or care to know how stocks will perform over the next 5 years.

“But Dream Like an Optimist”

At some point, though, I need to start thinking long-term like an optimist. This isn’t some soft, subjective desire to “be positive.” It’s a factual, data-backed requirement. It’s “if you’re still a pessimist, you’re being foolish.”

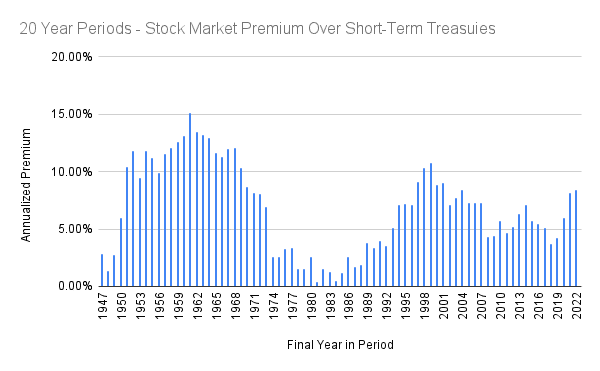

Because over sufficiently long periods of time, investing in stocks is the only reasonable option. Over 20- and 30-year periods, Treasury bonds have NEVER outperformed stocks.

And as we showed earlier, even over 5- and 10-year periods, it’s been rare for Treasuries to outperform stocks.

To me, the conclusion is clear: all of my long-term investing dollars need to be invested in stocks.

Where’s the Line?

The challenge becomes where we draw the line between short-term planning pessimism and long-term dreaming optimism?

If we draw the line too close to the present day, we introduce significant sequence of returns risk into our retirement plan. If we draw the line too far in the future, we hamstring our expected returns by leaning too far into stability (bonds), too far away from growth (stocks).

We need to find the right balance between where the numbers guide us vs. how we feel about our investment risk (or lack thereof). This isn’t a new challenge for investors. Same as ever.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!