Commission – the act of committing. Doing something.

Omission – the absence of action. Doing nothing.

I like George Carlin. He’s brilliantly funny. But I’ve always had an issue with his jokes about voting. I couldn’t quite put a finger on my issue, though…

“You caused the problem. You voted them in. You have no right to complain. I, on the other hand, who did not vote, who, in fact, did not even leave the house on Election Day, am in no way responsible for what these people have done, and have every right to complain as loud as I want about the mess you created that I had nothing to do with.”

George Carlin

That’s funny! But I recently realized my issue.

Carlin suggests that omission, by default, absolves us of responsibility. I don’t agree. And I’m not the only one.

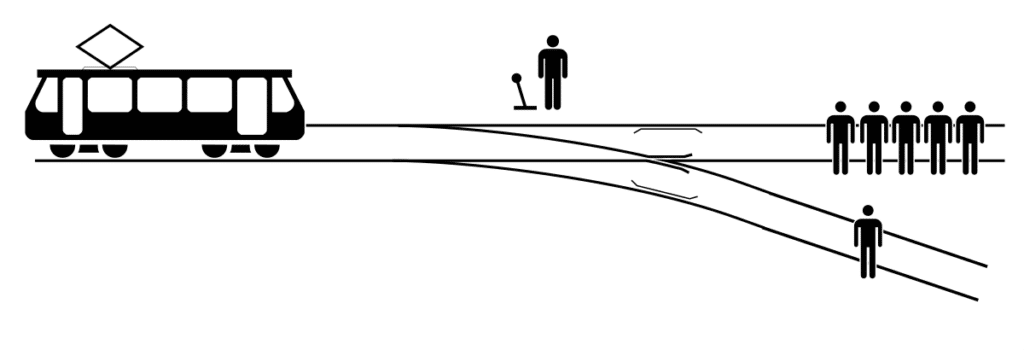

This brings us to “the Trolley problem,” perhaps the most famous conundrum in philosophy.

You watch as a train heads down the tracks, straight toward five strangers tied to the rails. You can’t possibly run down to the tracks in time to help them. But you can reach the track switch to divert the train to an alternate track.

There’s one problem

Another stranger is tied to the alternate track. Just one stranger.

What do you do?

If you do nothing – omission – the train kills five strangers. But you didn’t tie them there. You are nothing more than a coincidental bystander. Why should you feel any guilt?

If you pull the switch – commission – you save those five lives. But you also play “executioner” for the poor sap on the alternate rail. You are no longer a bystander, but taking an active role – including an active role in one poor guy’s death.

Omission kills five. Commission kills one. What should you do? We won’t try to answer it today.

But we can say this: both omission and commission have their costs. It might feel like omission bears less guilt. But that’s just your feeling. A biased feeling at that. Those five dead guys really wish you had chosen to act.

In fact, this biased feeling is well-documented and aptly named the omission bias.

I recently listed to Joel Laarsgard (from How to Money) and Ben Miller (from ChroniFi) discussing a bunch of different financial ideas on Ben’s podcast (their full conversation below).

I loved how they framed omission and commission in personal finances.

Investing is an act of commission. You choose to put your money at risk. Sometimes your capital grows. Sometimes it doesn’t. The commission of risk-taking leads to gains and losses.

Omission is the decision to not invest. Typically, one deposits their money into a savings account at the bank. No risk. No gain. No loss.

Or is there? Is there really “no loss” from omission?

Because when I compare a couple basic investing strategies (commission) to not investing at all (omission), I like the results from commission.

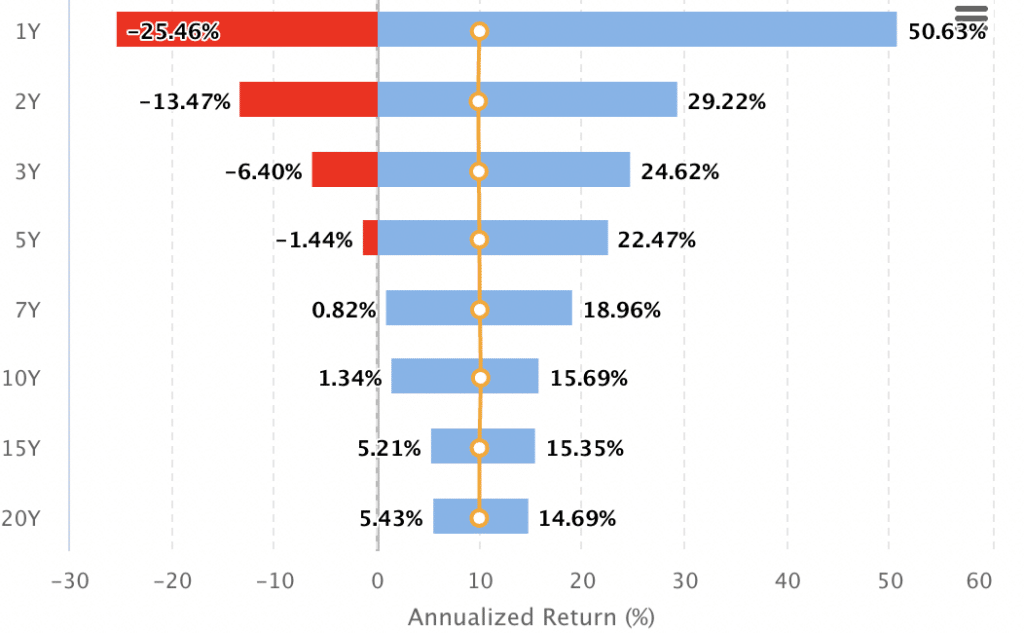

Let’s look at a 60/40 portfolio over the past 50 years: 9.9% compound annual growth rate with no 7-year periods of negative performance.

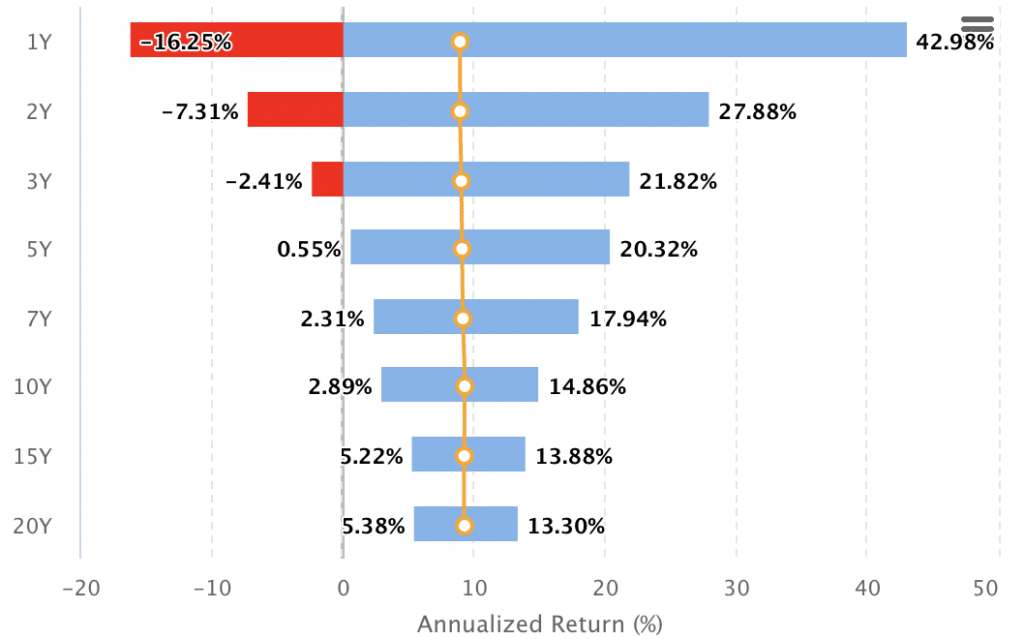

Next, the 40/60 portfolio: 8.9% compound annual growth rate over the past 50 years, with no 5-year periods of negative performance.

And over that same 50-year period, savings accounts (as measured by the Federal Funds rate) returned an average of 5.0%.

But wait!

Because over these same 50 years, we’ve seen an average inflation rate of 3.9%, slowly eroding the value of our dollars.

Meaning the real returns of these three simple investments are:

- 60/40: 6.0% per year

- 40/60: 5.0% per year

- Savings accounts: 1.1% per year

Commission – even in a milquetoast 60/40 or 40/60 format – provided 5-6% real returns per year, magnifying someone’s spending power by over 1100%.

Was it a bumpy ride? Sometimes. But a long-term investing mindset cures that.

Omission, meanwhile, provided a 1.1% annual real return, increasing spending power by 72%.

Omission has no loss? Omission absolves us of responsibility? No way.

I know what I’m voting for.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!