It’s a story as old as the stock market: Girlfriend has serious doubts about brazenly confident investing Boyfriend.

I recently participated in a conversation on Reddit where a young woman was seeking rational arguments against her investment-loving boyfriend. She was pretty sure there were some hints of smoke, but Girlfriend was wondering if, indeed, there was fire. I’ll highlight some of the important facts from Girlfriend’s description.

- “Investing Boyfriend thinks he can research his way to predicting individual stock performance (he’s not in any related field whatsoever- didn’t study investing or anything).”

- “He thinks index funds are too safe and that you need to take risk on individual stocks to succeed.”

- “This is his retirement strategy.”

- “He also lost 10K last year (2019) but thinks writing it off makes it okay.”

We’re going to address all of these ideas later on, but let’s start with the first two.

How to beat an index fund

A simple investing equation is Profit = Performance – Fees. The money you make (Profit) is equal to the change in your investments’ value (Performance) minus your investments’ Expense Ratios or trading fees (Fees).

As we’ve discussed before on the Best Interest, an index fund essentially promises you average performance with close to zero fees.

If you’re going to beat an index fund via active trading, you’ll be accruing transaction fees. Active trading = lots of trades = lots of trading fees. Your performance, therefore, needs to be well above average. Although I will admit, competition in the financial industry is driving the fees from trading way down.

So maybe you won’t be actively trading, but instead you’re going to give an investment professional your money. In that case, you’ll be paying that professional an annual fee for their services. Again, they’ll need above-average performance to justify their above-zero fees.

But the facts don’t lie. Most people will not be “above average enough” to justify the investment fees that their strategy suffers from. Why is that? I read a terrific answer recently in the book The Signal and the Noise, which I highly recommend. Author Nate Silver quotes Henry Blodget:

“Everyone thinks they have this supersmart mutual fund manager. He went to Harvard and has been doing it for 25 years. How can he not be smart enough to beat the market? The answer is: Because there are nine million of him, and they all have a 50 million dollar budget and computers that are co-located in the NY Stock Exchange. How could you possibly beat that?”

Do you think investing Boyfriend is going to “beat that?”

Investing Boyfriend’s rationale

Girlfriend listed out additional points that Boyfriend makes to support his case. We’re going to go through, point-by-point, to counter Boyfriend’s thought process.

401ks are too safe. You shouldn’t put in more than a company match. Index funds, mutual funds, those are all too safe. To make money you have to invest in individual stocks

“Safe” here is a fairly subjective term.

And, to be perfectly clear, a 401(k) is simply a tax-advantaged investment vessel. It’s the investments within the 401(k) that are either risky or safe.

If you can afford to, you should absolutely put more money into your 401(k) that the company match. Since you don’t pay taxes on the money going into a 401(k), it’s like you’re getting an extra 20-30% for free.

Boyfriend is making the argument that index funds are too safe. And we’ve already talked about this. Index funds, by definition, have average performance and zero fees. Whether that’s too safe for you is a matter of personal risk posture.

You should be using your IRA to take more risk

An IRA, or individual retirement account, is a blanket term describing a few different types of non-401(k) retirement accounts. That is, they are taxed differently than 401(k) accounts.

A Roth IRA, for example, can be thought of as the “opposite” of a 401(k). For a Roth IRA, you pay normal taxes up front when you invest your money. But when you pull that money out at retirement, you owe no taxes.

Now, the actual point: should an IRA be used to take more risk? I’d have to hear a compelling argument about why this is the case. Perhaps investing Boyfriend’s specific tax scenario makes more sense for him to use his IRA for higher risk.

My personal choices share an equal amount of risk across all of my investing accounts.

I doubled my investment I made on ______ last year, but then the markets crashed last December (2018) and wiped it

True skill in the market describes the ability to both buy and sell at the right time. Boyfriend’s argument here is, “I chose a great stock to buy, but then I didn’t sell it before it crashed.”

Well…there’s your sign. Timing the market is a loser’s game. And Boyfriend lost.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

“Low risk, low reward”

Specifically, investing Boyfriend is criticizing index funds here. It’s wrong. Instead it should be:

Average risk. Average reward. Zero fees.

I pick stocks with dividends, so I keep making money

Dividends? Some more established companies will literally give a percentage of their profits to their stockholders. It’s called a dividend. Typically, newer and growing companies will choose to re-invest their profits into the company, and will not pay a dividend.

As an example, Uber–which is still trying to grow–doesn’t pay a dividend, But General Motors–which is established–recently paid about a 4% dividend in 2019, or $1.50 for each $35 share.

If picking only dividend stocks was the key to making above-average profits, why wouldn’t everyone already be doing it? Why would anyone invest in Uber if they were guaranteed to be below-average?

Not to mention, if an index fund comprises dividend stocks, then people owning that index fund will get still get the dividend benefit. Index funds and dividend stock are not mutually exclusive.

You can just write off the losses

While true–tax-loss harvesting eases the pain of investing losses–I still think that Warren Buffett is blowing a fuse right now. Why? Let’s go back to Buffett’s two simple rules of investing.

Rule #1: Don’t lose money.

Rule #2: Never forget rule #1.

Writing off investment losses is not a good reason to lose money. You still lost money!!!

“He also lost 10K last year (2019)…” —Girlfriend

This isn’t a very scientific thing of me to say, but sometimes cherry-picked data makes the biggest statement.

How does someone lose money when the S&P 500 is up 30% and the Dow Jones is up 24%?

I’d remind you: a monkey could have picked random stocks in January 2019 and would have made a ~25% profit over the year. And you know that I dislike giving credit to banana-stealing monkeys.

It’s one thing to underperform a 25% profit–say, by only making a 20% profit. But to lose money–to make a negative profit–when everyone else did so well? That’s really, really bad.

I just need to get better at deciding when to sell

And if I want to get into Hogwarts, I just need to get better at my Potions.

This is very close to saying, “If I was better, then I’d be better.” And that just don’t make no sense.

“This is investing Boyfriend’s retirement strategy”

Yikes. This is a scary one. While I understand the allure of taking one’s destiny into one’s own hands, it helps to know what you’re doing.

I like to think I’ve got a good handle on my retirement plans. Not only does the idea of stock picking feel risky, but it also feels so stressful.

Do I want to spend time, effort, lose sleep, etc. because I need to be better than millions of other investors at deciding whether GM is undervalued? Whether Uber has peaked, or if it’ll keep going up? If I should start selling my investments in anticipation of the coming recession? This sounds really stressful!

I like my no-stress, average performance, Lazy Portfolio method.

Summary

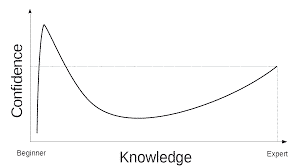

While investing Boyfriend and I have our subjective differences, I also think that some of his views are objectively, factually wrong. And while I cannot say this with any certainty, it sounds like he might be amid the early stages of the Dunning-Kruger curve.

His confidence seems pretty high, despite lots of evidence pointing to his lack of understanding. For both his benefit and Girlfriend’s, he should keep learning, thus moving further right on the Dunning-Kruger curve. Soon, his confidence will start to match his knowledge–that is, both pretty low. And for the sake of their personal finance, that’s a pretty good thing!

What do you guys think? Is there a investing Boyfriend or Girlfriend in your life? It’s ok, your secret is safe with me.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

-Jesse Cramer

The opinions we’ve heard about investing are all over the place. Some very strong against “the stock market” because their parents were burned by single stock investments back in the 80’s and 90’s (before index funds were common for individual investors), so they learned to not trust it. It’s unfortunate that workplace retirement plan paperwork doesn’t typically cover this stuff either (that a 401K is just the bucket to put the eggs in).

It’s funny, of course the odds are boyfriend is going to have a terrible retirement unless he adopts a sounder philosophy. But, you know, there is a tiny shred of a chance he’s the next Warren Buffett and forty years from now he’ll be the first person to be worth one hundred trillion dollars. That’s the problem with statistics, they tell you everything about a large group of subjects but they tell you absolutely nothing about an individual. There are a lot of very rich people that got that way by buying individual stocks, I’m not one of them, I’m fine with index funds myself, but still, I bet there are a thousand future billionaires out there right now that look just as dumb as boyfriend.

Fair point, Steve! I agree with everything you’ve written. I wrote about something just like this in my “Risk Posture” post.

Pingback: Index Fund Bubble: Arguments For and Against - The Best Interest