Would you rather listen to this? I discuss this article in Episode 42 of Personal Finance for Long-Term Investors (formerly The Best Interest Podcast), below.

Friend-of-the-blog Tyler knows I like a good math problem, so he asked me:

Question for you about paying off debt. Many people know about the “debt snowball” and the “debt avalanche.”

But I wonder if focusing on the debt that is costing you the most based on the rate and balance would have an advantage over just focusing on paying off the smaller balance with a higher rate?

First, let’s define some terms:

- The “debt snowball” is an idea that you should focus on your smallest debt principal first.

- The “debt avalanche” suggests focusing on your largest interest rates first.

- And Tyler’s idea—I call it the “debt blizzard”—focuses on whichever debt has the largest monthly payment first.

The table above aligns with these definitions (see the three columns on the right).

But, which method is mathematically best?

Surprise! Did you see the article title!? It’s the debt avalanche. Always. No matter what. Speaking of…did you see this crazy avalanche video?!

If you want to understand why, follow this logic:

- All three methods eliminate the total loan principal. We need to find whichever method minimizes the interest paid. Do you agree?

- So let’s say I give you $1.00. Just one. You decide to pay off some debt. Two things will happen:

- You’ll decrease your remaining principal by $1.00

- You’ll decrease your future interest payments by…well, we’d have to do some math.

- But if you want to be most effective with that dollar, how would you do it? No matter which debt you target, you’re always decreasing your principal owed by $1.00. That’s not a differentiator. Your only “knob to turn” lies in the interest payments.

- What’s the smart move? You should target whichever debt lowers your future interest payments the most. Agreed?

- Well…that’s easy. In our example above, one debt is charging interest at 24%. That’s the debt we should target with this $1.00.

- Now repeat, dollar after dollar…

- As long as the 24% loan still exists, that one makes sense to target. Then the 8% loan, then 6%, then 4%.

- As we said at the beginning: All three methods eliminate the total loan principal. Our method minimizes the interest payments.

- We’ve just created the debt avalanche. That’s the optimal payoff plan.

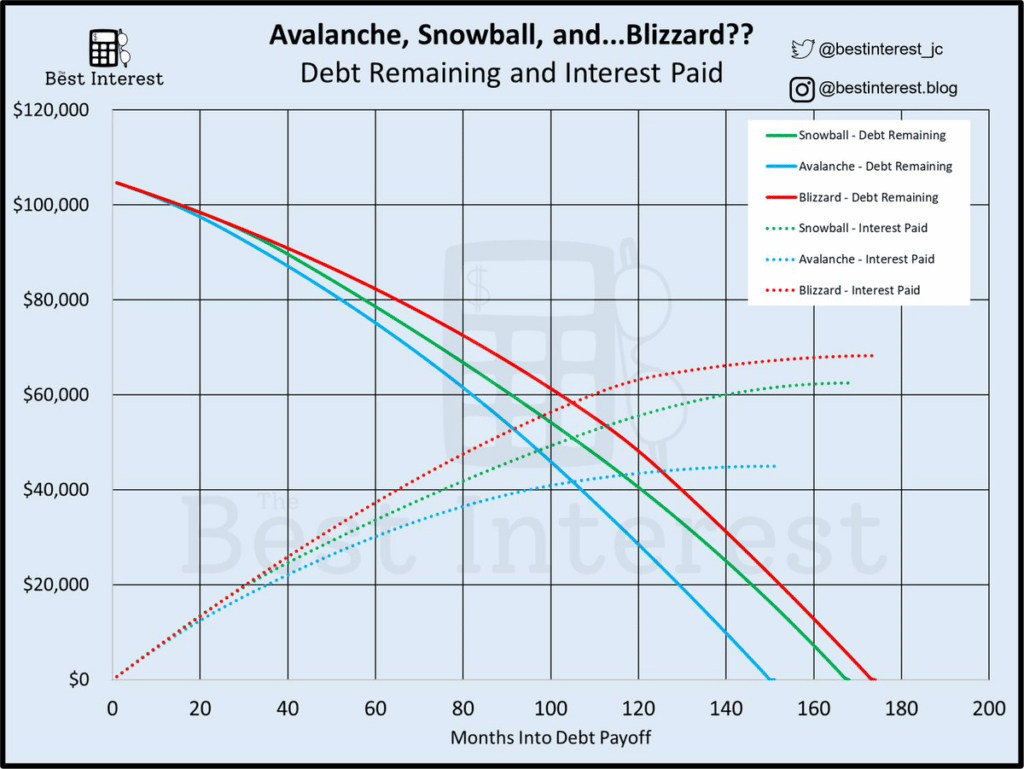

The chart above shows the exact payout schedule for our four loans using the three different methods (I assumed $1000 per month payments).

The solid lines track our debt over time. The dotted lines track how much interest we’ve paid.

The avalanche has both the shortest repayment period and the least interest paid.

The snowball’s and blizzard’s efficacies are dependent on the loans themselves. Sometimes they’ll work well, other times poorly. Because the snowball (which cares about principal) and the blizzard (which cares about monthly payments) are focused on the wrong metrics.

Yes – the snowball does have a non-financial benefit of “small wins.” By focusing on the smallest debt first, a person can build motivational momentum to continue their positive financial journey. This is phenomenal and could be a justifiable reason to use the debt snowball. The blizzard has psychological benefits too. But the avalanche would still be mathematically optimal.

Nothing ground-breaking here. But this should be helpful if you or people in your life are unsure how to approach paying off their debt.

Use the debt avalanche. Focus on the highest interest rates first.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

I’m surprised nobody talks about a hybrid approach to blend the psychological benefits and the optional financial benefits.

Let’s say you have 3 credit cards at various amounts and all are at a high interest rate but relatively close together (19%-21%). Then a car loan at 1.9%, and number of student loans between 4-5%.

Starting with the credit cards, then the student loans, then the car loan makes sense due to interest rates and will save a bunch of money. Starting with the lowest balance on the credit card (and then the next bucket when all credit cards are done) though can get you an easy win and not change the interest payments significantly as they’re in the same ball park.

There’s also a benefit to reducing risk, as completely paying off loans faster by reduces your minimum payment requirements and puts you in a less risky position in an emergency/job loss situation while reducing the risk of one quitting as they feel they’re not seeing progress fast enough. If we think of it like risk-adjusting a portfolio, we might have to consider if the extra risk is worth the small savings over the hybrid approach. Although certainly the savings would be worth it over the debt snowball.

I mostly agree with you, just providing an alternative perspective. My method is harder to explain and counts on the individual to be able to make the right judgment as there’s no black and white rules.

Thanks for the thoughts, Joe – I appreciate it!

Yeah, the “risk reduction” aspect of eliminating minimum payments is definitely worth considering and is probably worth me thinking about some more…

If you’re paying $1000/month, what value should you place on reducing your monthly payment fro $500/mo to $400/mo?

It’s got to be a related to the question, “What are the odds that you won’t be able to make $1000/mo payments in the future? And if that’s the case, how low will you go?”

Great food for thought.