Jesse – after a tough tax season for me, can you offer any advice on capital gains tax planning? Should I set up a tax witholding on my taxable accounts? What general framework should people use?

Jennifer, reader-of-the-blog

Great questions. Let’s devote an article to the basics of capital gains taxes.

My recommendation: skim the headlines in the article. Many of you know the basics already, but I bet certain sections shed new light for you.

What are Capital Gains?

A capital gain occurs when you sell an asset for more than you bought it for. A capital loss occurs when you sell an asset for less than you bought it for.

Capital gains or capital losses become realized upon such a sale. Until that sale, the capital gain/loss is considered unrealized, sometimes called “paper gains/losses.”

While realized capital gains are taxed…ew!…never forget: capital gains are evidence that something good happened!

How are Capital Gains Calculated? What Accounting Methods Are Used?

In their most simple form, capital gains are synonymous with “profit.” But three different accounting methods can be used to calculate capital gains.

Imagine the following scenario:

- You buy 100 shares of Fund A for $100 each in the year 2000

- You buy 100 more shares for $150 each in 2005

- You buy 100 more shares for $300 each in 2010

And today, with the fund price at $400, you want to sell 50 shares. What’s your profit? What’s your capital gain?

The first in, first out accounting method assumes you’re selling the oldest shares first. All 50 shares would be sold from the lot with $100 original price (or “cost basis”) resulting in $300 capital gains per share, or $15000 total capital gains.

The specific share identification method involves, as the name implies, identifying which shares are to be sold. To keep taxes low, I might choose to sell 50 shares from my 2010 purchase lot, resulting in a $5000 capital gain. But since I’m identifying specific shares, I need to ensure I’m keeping excellent records.

Or I could use the average basis method. The average cost of these shares is $183.33, resulting in $216.66 capital gains per share, or $10,833 in total capital gains. Once this method is used, all remaining unsold shares get reconstituted to a cost basis of $183.33.

The average cost basis method is generally NOT applicable to individual stocks. Instead, it’s applied to mutual fund and ETF purchases.

How are Capital Gains Taxed?

Capital gains are subject to tax when in taxable accounts. There are no capital gains in 401(k), IRAs, HSAs, or any other “qualified” or “tax-advantaged” investing accounts. =

The first major consideration in determining capital gains tax is the duration of holding the asset.

- If you hold an asset for less than a year before selling it, it generates a short-term capital gain/loss.

- …more than a year, it generates a long-term capital gain/loss.

Short-term capital gains are taxed as normal income. For many Americans, this equates to a 12% to 24% tax rate. Here’s more on how Federal income tax brackets work.

Long-term capital gains are taxed from 0% to 23.8%, depending on the investors’ total income.

Importantly, capital losses offset capital gains. Going even further, capital losses can offset your normal income (up to $3000 per year), and excess capital losses can carry forward into future tax years.

What Assets Are Subject to Capital Gains?

The most common assets that are subject to capital gains are:

- Stocks

- Bonds

- Real estate

- Vehicles

Other reasonable capital gains assets include:

- Gems and jewelry

- Digital assets, like virtual currencies, stablecoins, and non-fungible tokens (NFTs)

- Household furnishings

- Gold, silver, and other metals

- Coin and stamp collections

- Timber grown on your home property or investment property

How Are Long-Term Capital Gain Taxes Calculated?

Long-term capital gains are taxed based on a tax filer’s taxable income, not just based on their capital gains alone. As a reminder, taxable income includes many sources, including:

- Wages, salary, commissions, bonuses, etc.

- Unearned income, such as canceled debts or government benefits.

- Capital gains themselves, as well as investment dividends and interest

It’s important to understand, for example, how capital gains taxes interact with Roth conversions and other retirement tools.

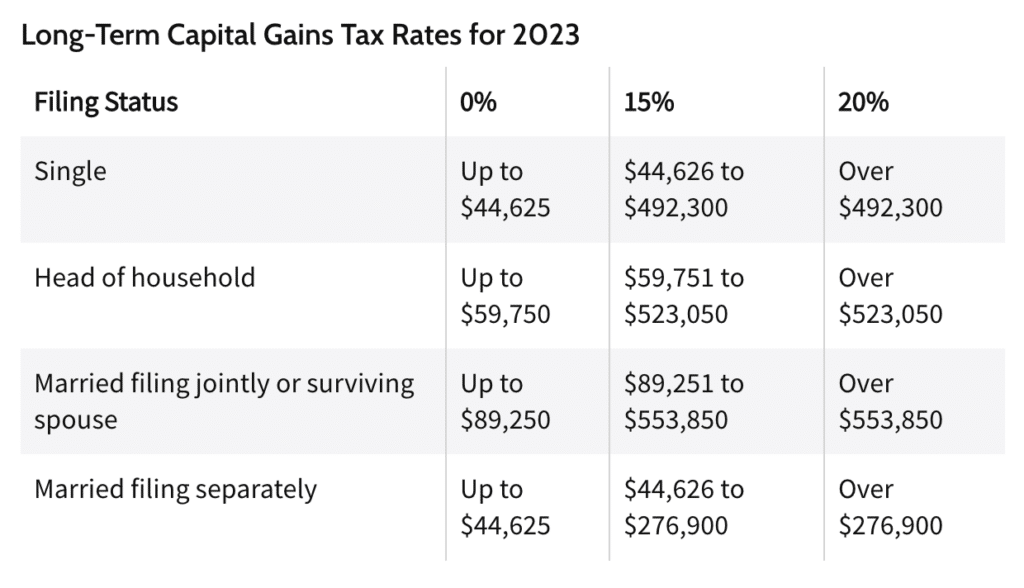

The capital gains brackets for 2023 are as follows:

For a single filer, if their total taxable income falls below $44,625, they’ll owe nothing on capital gains. Nice!

The “taxable income vs. capital gains” idea confuses many people, who might mistakenly think, “My first $44,625 in capital gains aren’t taxed? Sweet!” That’s only true for someone with no other taxable income.

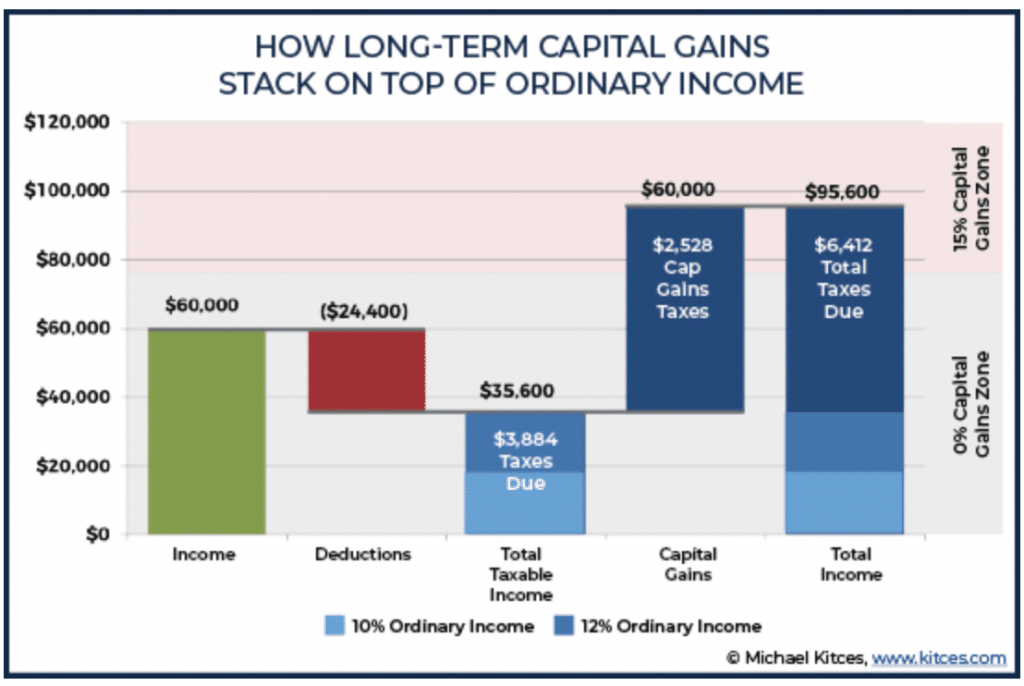

Other forms of taxable income push capital gains into higher tax brackets. This is commonly referred to as “stacking.” Financial planning blogger Michael Kitces has a terrific infographic to describe this stacking:

You can see how this person’s taxable income (Column 3) “stacks” below their capital gains (Column 5), pushing some of their gains into the 15% capital gains zone (see right Y-axis).

When are Capital Gains Taxes Due?

Normal income is withheld from your paycheck to make estimated tax payments throughout the year.

Capital gains are a bit different. We’ll cover the “withholding” idea below.

Nevertheless, you should consider making capital gains tax payments on a quarterly basis using estimated tax payments. In other words, you should not simply wait for the end of the year to make a large, lump sum capital gains tax payment. Instead, you should use estimated tax payments if:

- You’ll owe an estimated capital gains tax of at least $1000 for the year, AND…

- Your current year’s tax withholding will be less than 90% of what you owe this year, OR less than 100% of what you owed last year.

Example: Capital Gains Estimated Tax Payments

I’ll admit. Those clauses above are confusing. Tax code usually is. An example will clear them up.

Last year, John and Jamie earned $160,000 and paid $20,736 in Federal Taxes. This year, their combined salary is $170,000 and they’re on pace for Federal withholding of $22,936.

This year, in February, John and Jamie sell some assets for a $50,000 long-term capital gain. These capital gains all fall in the 15% bracket, incurring a tax burden of $7,500. Should John and Jamie make estimated quarterly payments?

- Do they owe capital gains of at least $1000? Yes.

- A) Is their current-year withholding less than 100% of what they owed last year? No. B) Is their current-year withholding less than 90% of what they’ll owe this year? Yes!

They’ll owe $22,396 + $7,500, but they’re only withholding $22,396. They’re only withholding ~75% of what they owe, which is under the 90% threshold. Because they’re under that threshold and they’ll owe more than $1000, John and Jamie should make estimated tax payments.

The payments are due quarterly and are due on April 15 (Q1), June 15 (Q2), September 15 (Q3), and January 15 (Q4). And yes, those 4 payment dates are NOT evenly spaced. I have no idea why…

Can I Set Up “withholding” for Capital Gains?

“Withholding” is a concept from the income tax world, when a final tax bill is predictable based on income. The capital gains world is not so clear.

Will there be more gains later this year? Will there be capital losses this year to offset gains? Will you even owe capital gains taxes, or will you fall into a 0% capital gains bracket?

For all these reasons, there is no “withholding” for capital gains purposes.

Instead, many investors elect to create a “DIY withholding” account to ensure they maintain enough cash to fully cover their capital gains tax burden.

What’s the Net Investment Income Tax?

The Net Investment Income (NII) tax is a relatively recent tax that effectively acts as an additional capital gains tax (at a 3.8% rate). NII tax applies to investment income above $200,000 (if filing taxes single) or $250,000 (filing jointly). Those thresholds mean NII applies to:

- A portion of the 15% capital gains bracket

- All of the 20% capital gains bracket

In other words, there are effectively (4) capital gains tax brackets: 0%, 15%, 18.8% (15 + 3.8), and 23.8% (20 + 3.8)

How Should I Minimize/Avoid Capital Gains Taxes?

I’m going to keep these tips brief.

- Take advantage of tax-deferred investing accounts.

- Invest for the long-term. Avoid short-term capital gains tax rates.

- Try to offset capital gains with capital losses.

- Utilize tax-loss harvesting and carryover losses to future years.

- Utilize tax-gain harvesting in low-income years.

- Use the best accounting methods for your situation.

- Wait to die. Seriously. (see below)

- Asset location – place your high-tax investment in qualified accounts and place your low-tax investments in taxable accounts.

- Use high-gains assets for your donations. The charity gets full value, you pay no capital gains taxes, and you get a tax deduction.

- Use high-gains assets as loan collateral. Many brokerage firms offer loans against shares, providing cash liquidity without selling the underlying shares.

What If I Die? Who Pays Capital Gains Taxes?

Under current tax law, if you die and leave high-gains assets to your heirs, no capital gains tax will be paid on the transfer. Not by your estate, nor by your heirs. Not only that, but your heirs will receive the assets on a “stepped-up basis.”

If you bought Apple in 2000, it was less than $1 per share. Today, it’s $166 per share. If you sold today, that $165 gain per share is subject to capital gains.

But if you die today, your heirs inherit those Apple shares at a $166 cost basis. If they sold tomorrow (at $166), there would be no gain, and therefore no tax.

For this reason, capital gains tax planning is especially important in retirement and older years. Should you sell assets and incur taxes? Or just wait to die?

Granted, this area of the tax code is hotly debated and in the legislative crosshairs. In general, capital gains taxes (a.k.a. taxes on capital) are significantly lower than income taxes (a.k.a. taxes on labor).

Questions?

Did I miss anything big? Got any questions for me? Fire away!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!