Highlights:

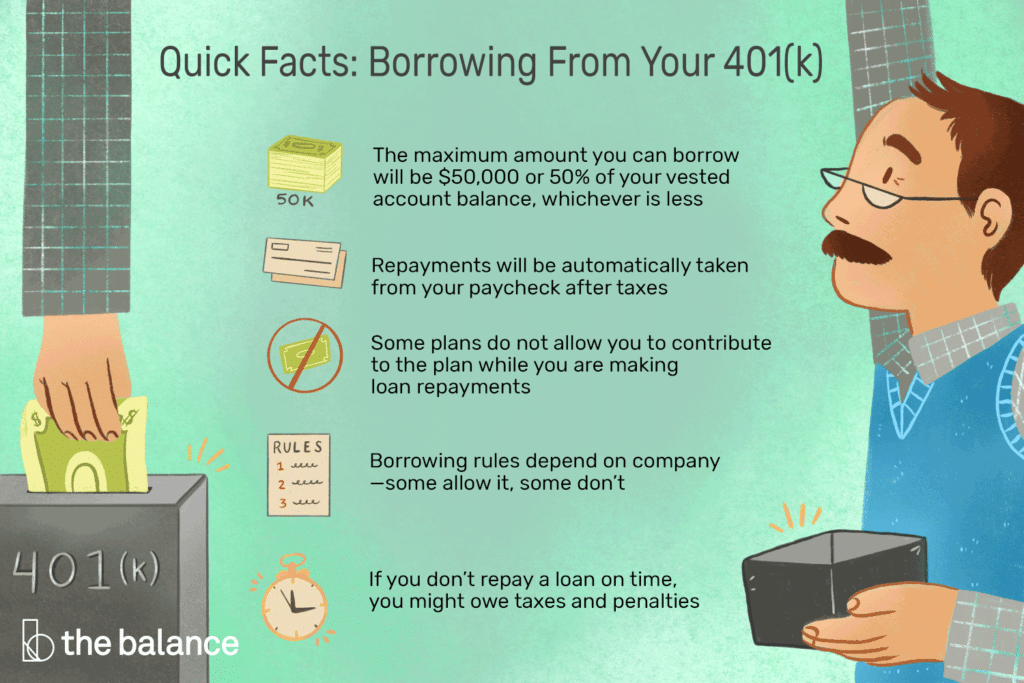

- 401(k) loans allow participants to “borrow” $50,000 or 50% of their 401(k) balance (whichever is less) from their own accounts

- 401(k) loans typically come with up to 5-year repayment terms and include “interest,” or additional repayments above what was borrowed, paid into the participant’s 401(k) account

- While 401(k) loans typically hurt the long-term performance of the 401(k), they can be a useful tool at times with a benefit that outweighs the cost

What is a 401(k) Loan?

First off, they’re not true loans. Instead, a 401(k) loan is a payment from you to you; from your 401(k) account into your bank account. IRS code permits you to access $50,000 or 50% of your 401(k) balance – whichever is less – on a tax-free basis.

You then have 5 years to repay your 401(k) account in such a way that it’s approximately in a state as if the loan had never occurred. These repayments are made as payroll deductions and are tax-free. There are also “interest” – or extra – payments beyond the original borrowed amount.

However, this “interest” is, again, going from you to you; from your bank account into your 401(k) account. It’s not like true loan interest, which is a payment you never get back.

These “interest” payments are, however, made with after-tax dollars. They’ll then be taxed a second time upon eventual 401(k) withdrawal. As such, these interest payments are “double-taxed” and can be thought of as a “fee” or inefficiency of 401(k) loans.

A typical 401(k) loan might borrow $10,000, charge 5% interest, and be repaid in 2 years. The interest payments would amount to ~$750 over those two years, taxed at your current income tax rate. While such a double-taxation “fee” is not ideal, it’s most likely much better than the interest rate and other fees charged by a private lender.

When Do 401(k) Loans Make Sense?

401(k) loans only make sense for amounts under $50,000 and for short-term needs. As long as a 401(k) loan is short-term, it should have little effect on your retirement plans.

However, the effect is most likely to be a negative one. Why? Because the market goes up more than it goes down and you’ll likely miss gains – not losses – while your money is out of the market.

Example: you borrow $10,000 and plan to repay it over exactly one calendar year. Your 401(k) plan dictates you repay the loan with a 5% interest rate. Meanwhile, the market grows at 1% per month throughout the loan period. What’s the total cost of your loan?

If you hadn’t taken the loan, your $10,000 would have grown to $11,268, all of which are pre-tax dollars.

Instead, after the loan, your 401(k) stands at $10,968 – about 2.6% less. Roughly $271 of the balance is “double-taxation” interest repayment dollars, representing ~$50 in additional costs.

The total fees/losses of this 401(k) amount to 3% over one year. All in all, that’s pretty good! Very few loans out there are so cheap. Not to mention, 401(k) loans have a reputation for being quick and convenient since there is no true risk assessment or underwriting. After all, you aren’t actually borrowing someone else’s money.

The Downsides of 401(k) Loans

401(k) loans should not be used, in my opinion, for long-term loans. For example, let’s run a similar analysis as above, except for a $50,000 loan over a 5-year term.

The untouched 401(k) would have grown from $50,000 to $91,000.

The loan 401(k) ends up at $78,300. Of that amount, $6,300 is “double-taxation” interest repayment dollars, representing ~$1300 in additional costs.

This total fee – 15-16% over 5 years – is still reasonable within the larger context of loan interest rates. But that’s a fairly steep fee to pay considering you are borrowing the money from yourself. Rather than suffer that 15% loss, I would ask you: is there another way you can finance your expenses without taking a 5-year loan?

Another potential downside…you might not be able to add new funds to your 401(k) until the loan is fully repaid. You might miss out on year(s) of use-it-or-lose-it tax advantages.

Another potential downside…you don’t want to leave your employer if you have an outstanding 401(k) loan. In other words, taking a 401(k) loan might “force your hand” to stay with your employer until it’s fully repaid.

If you leave your employer and fail to repay the loan in full, your loan will most likely be considered A) an early 401(k) withdrawal, suffering a 10% penalty, and B) a taxable event, thus subject to income tax.

Questions to Ask Before Taking a 401(k) Loan…

- Do I understand how my specific 401(k) plan handles 401(k) loans?

- What “interest rate” will I be charged?

- Based on my loan amount, what’s a reasonable timeframe to repay the loan?

- Can I make new contributions to my 401(k) while the loan is outstanding?

- Am I ok with the possibility that the market might take off while I have my loan, thus preventing me from realizing those gains in the market?

- What are my alternatives if I don’t take the loan? Would I pay higher fees elsewhere? Can I manage without taking any loan?

- How confident am I that I’ll stay with this employer until the loan is fully repaid?

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!