When I talk to new investors, I get questions like:

- What stock will go up 100% next year?

- I need to 10x my money this decade – how should I do it?

- I’m 32, just started investing, and want to retire by 40. What’s my next step?

These investors are cursed by exaggerated expectations, just like that stumpy kid in school expecting to play basketball at North Carolina.

Stumpy won’t go D1 (or play college ball at all, for that matter). But we can offer advice that will improve his game nonetheless. Get faster. Become a better shooter. Maybe he’ll contribute to the high school varsity team.

The new investors I outlined above are financial Stumpy’s. Their expectations aren’t grounded in reality. But we can help them nonetheless and reset their expectations. Everyone can improve their personal finances, even if they won’t retire by 35.

In this vein, the simplest starting heuristic is to compare an investor’s annual savings against their investment growth.

Back to 22

Nick is our 22-year-old test subject. He just graduated college and earns $40,000.

Following generally accepted wisdom, Nick saves 10% of his salary, or $4,000 per year. He invests that money in a total stock market index fund. His initial investment grows 5% in Year 1.

Nick’s annual savings = $4,000

His investment growth = $200 (5% of $4,000)

At this early age, Nick’s annual savings are far more consequential than his investment growth. Even if Nick found a magic stock pick that quadrupled his growth, he’d still only earn $800 of growth, or 20% of what he contributed himself.

What does this mean?

It means Nick should focus his energy on increasing his savings. That’s his quickest, easiest path to increasing his net worth.

Doubling his income gives Nick an extra $40,000 per year. Doubling his rate of return from 5% to 10% gives him a few hundred bucks.

It’s a no-brainer. Focus your effort where it has the greatest effect.

The Compound Snowball Rolls On…

But Nick’s story eventually changes.

By age 40, he’s doubled his salary ($80,000) and he’s investing 25% of it ($16,000 per year).

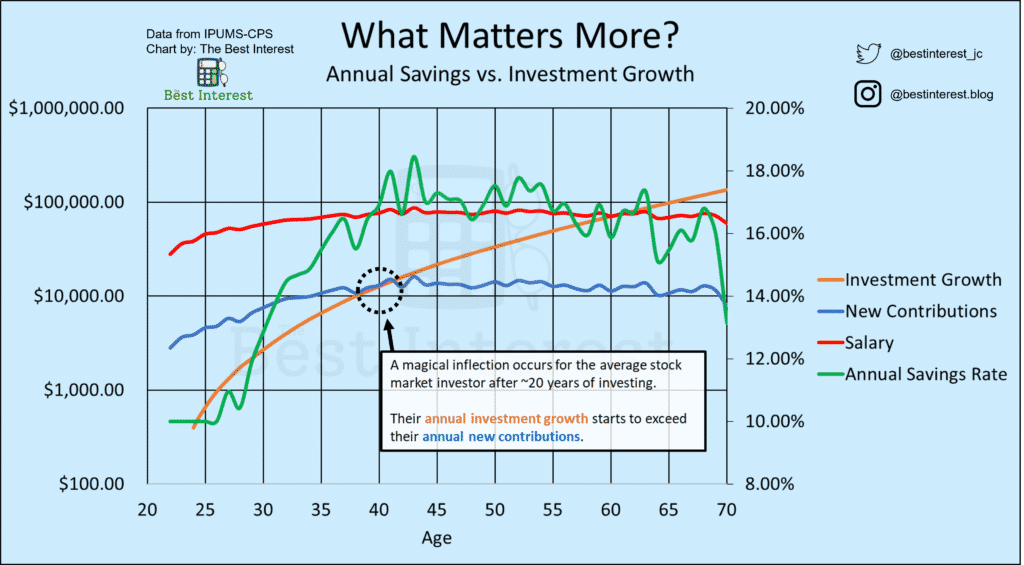

His portfolio has grown to almost $200,000, a far cry from his humble beginnings. And his total market index fund returns 8% this year, or $16,000.

Nick has hit an inflection point. His annual savings are equal to his portfolio growth (both $16,000). And with compound interest’s tailwinds behind him, there’s no going back. Nick’s portfolio growth will accelerate faster and faster, whereas his income growth will soon level off.

This story is plotted out in the graphic below. The graph uses average American salary data (in red), reasonable savings rate assumptions (in green as a percentage and in blue as gross dollars), and uses average stock market returns (in orange) to tell Nick’s story.

The average stock-centric investor hits Nick’s “inflection” after about 15-20 years of investing.

Before the inflection, their growth is dominated by their own contributions.

After the inflection, their growth is dominated by the compounding returns of their prior contributions. New contributions only play a minor role.

According to Nick Maggiulli (the inspiration for today’s investor, Nick) this inflection point should inspire a change in our money philosophy. And I agree with him.

Before the inflection point, Maggiulli says we should focus our energy on increasing our annual contributions. Build your career. Earn more money. Save a great percentage of that. This is how a young person grows their money.

At the inflection point, we should focus on energy equally between annual contributions and portfolio management. Both are important players in our net worth.

But after the inflection point, Maggiulli says we should focus more and more on portfolio management, less and less on new contributions.

Why? Just go back to the plot and look at age 60. Compare the blue vs. the orange line. Current investment growth dominates new contributions. So how do we focus more on the orange line? Through proper investment management and portfolio design.

We should carefully understand the risk and reward of our investment choices. We should plan a glide path into retirement, and how we’ll spend our money in retirement. Perhaps our investor, Nick, can do this on his own. Perhaps he needs professional help.

But the point is that Nick’s priorities needs to shift over time. The inflection point in today’s graph is Nick’s signpost. New contributions matter less and less. Stewarding the present portfolio matters more and more.

Inflection Reflection

I can’t tell you what stock is going up 100% next year or how to 10x your money this decade.

But even if you’re a complete stranger, your personal position on today’s graph helps me understand how to help you.

If you’re young and building, I’d tell you to focus on the long-term. Grow your career. Save as much as you can and “plant more seeds.” Earning 12% vs. 11% isn’t important right now. Instead, I’m better off telling you to forgo the $8,000 dirt bike.

If you’re older and established, I’d tell you to focus on your portfolio design. You’re not seeking to maximize return, but instead ensuring your portfolio is constructed to meet your goals. The returns will come, and they’re likely to eclipse any new money you can add this year. If your portfolio is growing by $100,000, it doesn’t really matter whether you add $10K or $15K of new money this year.

It’s that simple. Focus your effort where it has the greatest effect.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!