On a recent episode of Freakonomics, author Yuval Noah Harari** said:

Viruses exist whether we believe in them or not. Even if you don’t accept the stories about viruses, they can still kill you.

Yuval Noah Harari

🚨 This is not an article about viruses 🚨

But it is about science. Namely, I want to describe nine scientific facts that can help you achieve your personal finance goals in 2023. I hope you employ some of these ideas, because the science is true (whether you believe in it or not).

**Harari’s most famous book, Sapiens, is a must-read. It’s one of the few books I’ve read more than once in the last decade.

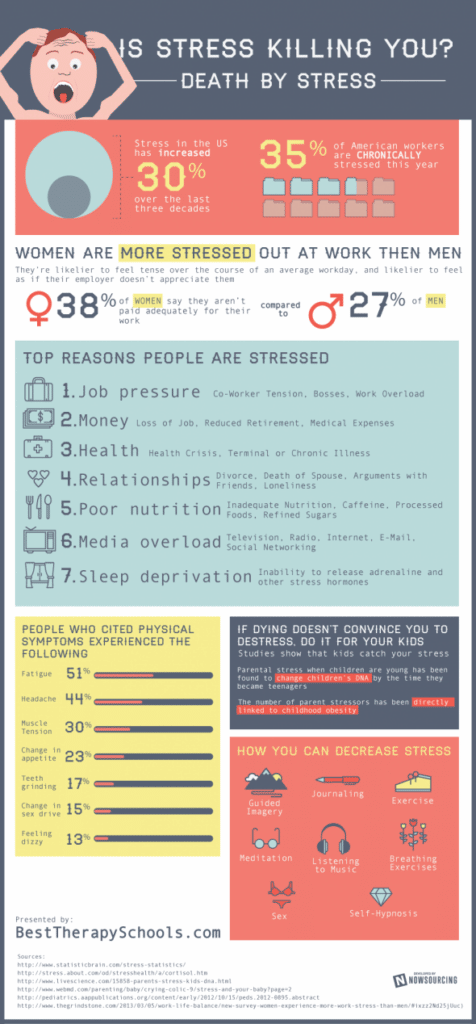

Financial Stress is a Killer

The science: stress is a killer, and finances are one of (if not the greatest) causes of stress in our lives.

The tip here is simple: do what you can to reduce your financial stress. The remainder of this list will help you do that.

Invest in Knowledge

The science: Ongoing education is a gold mine. Not only does new knowledge help you make smarter decisions, but education provides the confidence to take action.

So – how do you educate yourself on personal finance and investing?

Here’s my method. Every week, I read dozens of financial articles and listen to 10+ financial podcasts. I’m a nerd for this stuff and I do it professionally. But you don’t have to be as nerdy as me.

Because I share the best content I find in my quick weekly email. As of now, just shy of 6000 people read that email every week. You can sign up below. Not a bad way for you to learn, right?

[mc4wp_form id=”3254″]

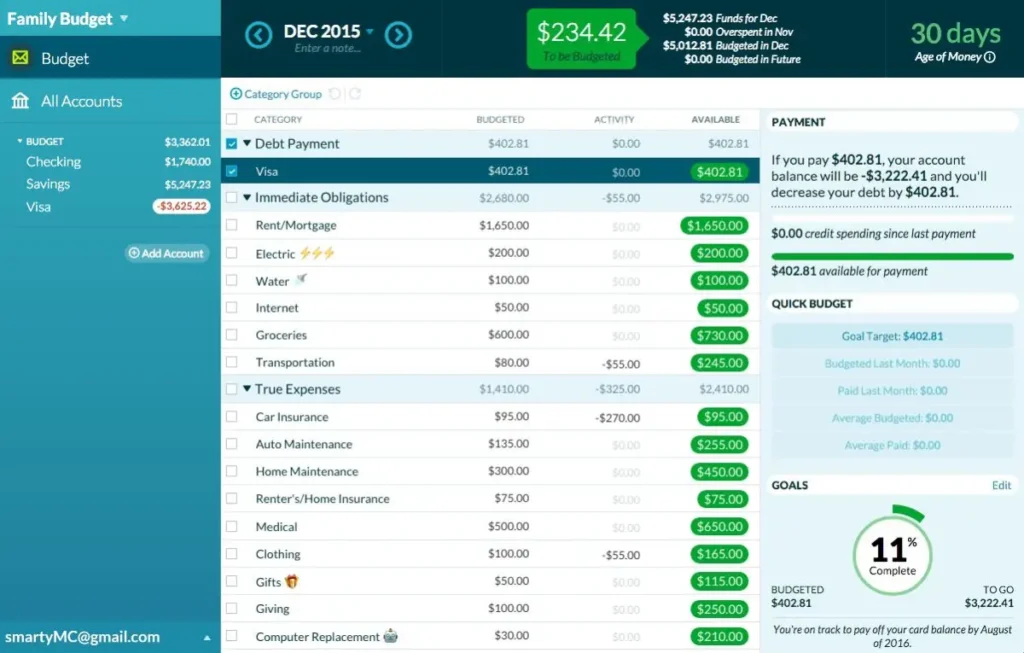

Measure First

The science: data-backed and data-driven decisions lead to better outcomes than simple gut feel.

I don’t write about budgeting much anymore. But I still maintain my budget on a weekly basis, measuring my spending, my earning, and how my accounts are changing over time.

Why? Because “you can’t manage what you don’t measure.” The best way to measure your personal finances is with a budget. Personally, I use YNAB for my budgeting. [You can use that link to get two months of the app for free]

But here’s some “counter science.” Whatever budgeting method you use, make sure it’s simple enough that you can maintain the habit. It’s better to be dedicated to a 90% solution than to burn-out on a 100% solution. YNAB is, admittedly, more detailed than some people prefer.

Other ideas include Mint.com, using a simple spreadsheet, using your bank’s budgeting solution, or recording via pen and paper.

Be SMART

The science: if you set goals, you’re more likely to reach them when you make them “SMART” (if you don’t set goals, focus on habits instead – see below for more)

The SMART acronym stands for Specific, Measurable, Attainable, Relevant, and Time-based. Your goals should tick each of those five ideas.

“I want to be better with my money,” is not a SMART goal. No S, no M, no T.

Nor is, “I want to save more,” nor “I want to budget.”

But “I want to save $6000 in my IRA in 2023,” is a SMART goal.

“I want to update my budget on the 2nd and 4th Sunday every month in 2023,” is a SMART goal.

Habit Formation

The science: Habits make or break us. This quick article covers the basics of habit formation perfectly.

Personal finance, like many New Years’ Resolution-y behaviors, are largely a function of stopping bad habits and forming good habits. Perhaps the most hyped book of 2021 was James Clear’s Atomic Habits. So hyped, in fact, it turned me off. It’s obviously overhyped…

But then I read it, and…yeah, it was really good. It’s a great resource to help you improve your habits.

This video/podcast is a another great habit resource:

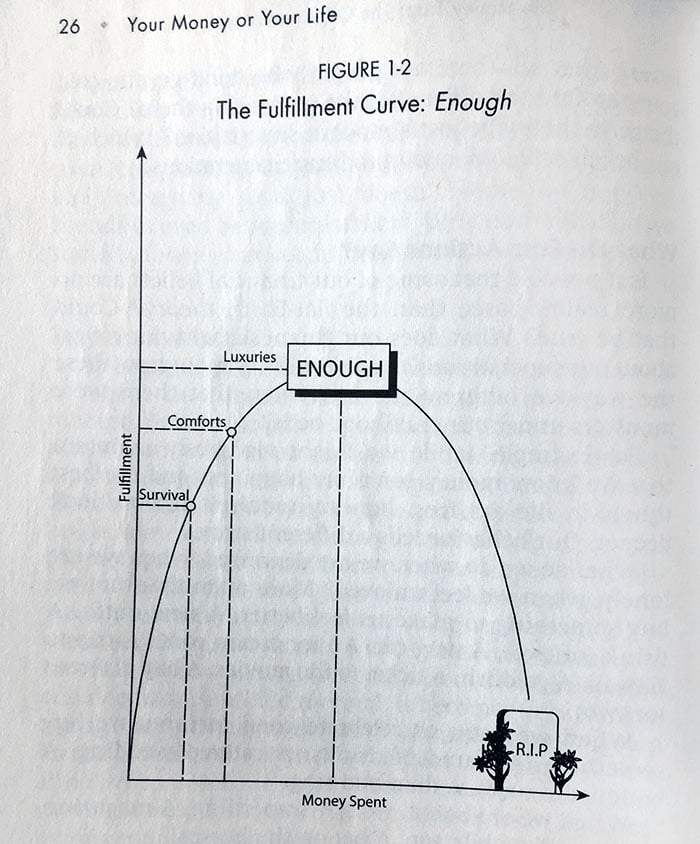

Understand the Fulfillment Curve

The science: our happiness-per-dollar eventually plateaus. More money doesn’t make us any happier. And our happiness-per-“stuff” eventually decreases, meaning that filling our lives with more material goods eventually makes us unhappy. This is called the fulfillment curve.

Once I internalized this idea, I began viewing personal finance in a different light.

My goals are not “make the most money” nor “buy the most stuff.” [Hey! Those aren’t SMART goals anyway!]

Instead, my goals are:

- Maintain a lifestyle at $ABC per year, because I believe that’s where my happiness plateaus.

- Actively avoid buying too much stuff, because I know that more stuff leads to stress**

**This stress presents as thoughts like, “My house is so messy,” and “I’ve spent my hard-earned money on this crap, but I never ever use it! What a waste!”

My recommendation: understand how the fulfillment curve fits into your life.

Be Automatic

The science: The more decisions we make, the worse we are at decision-making. Our brains only have so much “decision-making bandwidth.” This is called decision fatigue.

What to do about this? Automate your financial decisions.

- Set up automatic contributions to your 401(k), IRA, brokerage account, and/or other investing accounts

- Set up automatic bill pay. (Though there’s one exception, in my opinion. Don’t automate bills where you might want/need to negotiate or argue a bill’s amount. You don’t want to pay a company automatically, then turn around a day later and say, “Hey – I paid you too much!”)

Not only will you become a better saver, but automation helps prevent costly mistakes (like forgetting to pay your power bill)

Social Media Is Probably Hurting You

The science: Social media intentionally plays with your emotions with the end goal of serving you advertisements for products it suspects you’re interested in.

But Jesse, this advice is clearly confirmation bias because you recently quit social media.

Maybe? But that doesn’t mean I’m wrong.

Q: How do social media companies make money?

A: Advertisers pay them.

Q: Why do advertisers pay them?

A: Because they are serving ads to social media users.

Q: Well how do the advertisers make their money then?

A: Social media users buy their products and services.

The whole point of social media, in other words, is to get people like you and me to spend our money.

I enjoy spending. But I don’t want my spending manipulated by social media algorithms. My brain isn’t strong enough to fight the algos. (No offense, yours isn’t either).

I’m not even touching the mental health repercussions from social media content (e.g. comparing your everyday self to an “influencer’s” dolled-up self) and the subsequent spending decisions we make from that.

Know Yourself, Know Your Brain

The science: Your brain is different than mine (…duh!)

My favorite example of this involves a friend-of-the-blog (who I’m leaving anonymous). He’s a good friend. And our brains work in polar opposite ways when it comes to finance and diet.

I’m a financial nerd with strong financial habits. But I’ve never maintained a healthy long-term diet in my life. I’ve probably gone through 20 two-week diets and always struggled to cross that next hurdle.

My friend is the opposite. He’s been dedicated to an incredible diet and workout regimen for close to a decade. He’s amazingly healthy and fit. But he’s struggled with overspending, undersaving, bad investing habits, etc. for his whole adult life.

My strength is his weakness, and his strength is my weakness. How can two people be so similar, but so different? Our brains are fickle.

My only recommendation is that you work hard (and trust me – it’s hard work) to understand your brain’s strengths and weaknesses. If it helps, ask trusted friends or family for feedback on how you operate.

Knowing yourself – “temet nosce” – is a key factor in self-improvement.

If you have financial goals for 2023 (and beyond), I hope these nine ideas help you achieve everything you want and more. Happy New Year!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!