There have been a few times in the past year of writing when I’ve seen something so intriguing that I immediately knew, “This is a blog post waiting to happen.” It occurred again over the Thanksgiving holiday when I saw a picture of the Fulfillment Curve.

Living by the Fulfillment Curve belongs on any list of simple financial goals.

Have you ever heard someone advise, “Money doesn’t buy happiness.” And then a second person responds, “Obviously, you’ve never been poor.”

Well, they both might be right. The Fulfillment Curve explains why. But we’ll come back to this idea.

Where does the Fulfillment Curve come from?

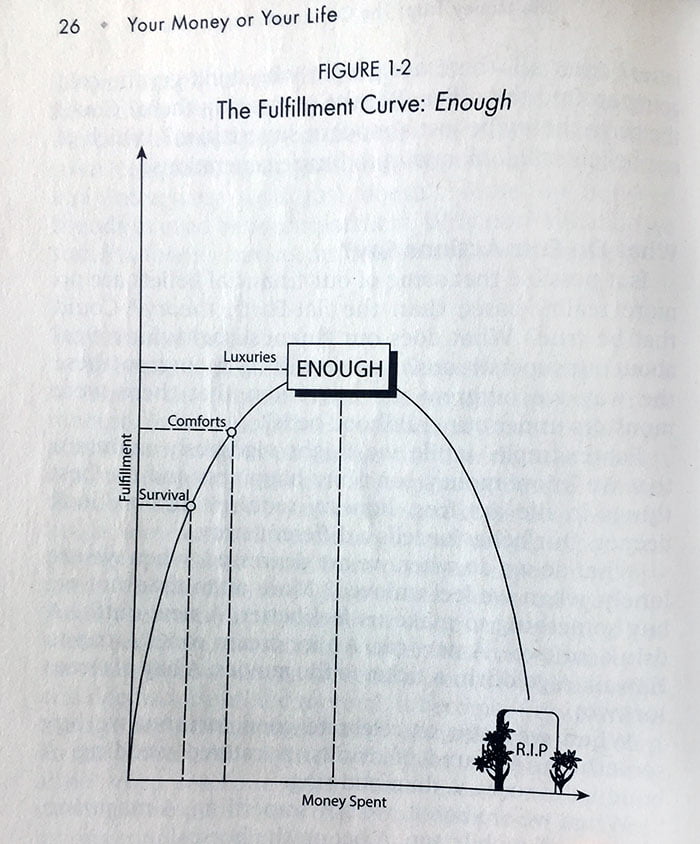

Before I go into the details of the Fulfillment Curve, how about giving credit where credit’s due? The Fulfillment Curve was originally described in the personal finance classic, Your Money or Your Life, by Joe Dominguez and Vicki Robin. Some people cite this book’s publication as the genesis moment of the FIRE movement.

The book goes beyond simple questions about earning, saving, debt, and spending. Dominguez and Robin also ask questions about fulfillment, goals, and life satisfaction. Sure, saving is good. But what’s the end goal? Paying off debt helps you. But why is it important in 10, 20, 30 years? Your Money or Your Life looks at the bigger picture. It’s a bastion of Best Interest thinking i.e. personal finance is a key factor in life satisfaction–but it’s only one factor.

In the authors’ words, many finance books written today “assume your financial life functions separately from the rest of your life.” But the point of Your Money or Your Life is “putting it all back together. It is about integration, a ‘whole systems’ approach to your life.” Good habits, good goals, optimizing satisfaction, maximizing free time, helping others, spending time with loved ones. Personal finance is a means to those ends, but those ends are the things we really care about.

Enough backstory: back to the main point. What’s this Fulfillment Curve?

Defining the Fulfillment Curve

In a single sentence, the main idea of the Fulfillment Curve is: there will come a point where more spending does not lead to more happiness, but actually does the exact opposite.

That’s right. Urban poet Notorious B.I.G. was rapping about the Fulfillment Curve when he opined, “Mo’ money, mo’ problems.” Thanks, Biggie.

Survival

Obviously, some spending is necessary. We need a roof over our head. We need sufficient food to maintain our health and nutrition. Speaking of health: medical expenses are a keystone expense. So are expenses related to getting to work, putting some clothes on our backs, and keeping the heat on in winter.

In short, there are some base level expenses that are key to survival. And the Fulfillment Curve recognizes this. The first chunk of our spending causes a huge shift in fulfillment, because maintaining the standards of survival is such an important and worthwhile use of our money.

Comforts

The next chunk of spending improves our lives further. Once we’re surviving, it’s nice to have a bit of entertainment, some flavor, the occasional treat. Add some spice to your plain rice. Buy a nice pillow so you don’t have a sore neck. Get a separate pair of boots for winter.

These things aren’t required, but they sure are nice. They make life more comfortable. This level of spending is far from opulent, but is a level above survival.

Luxuries

The final jump in spending that still improves our lives are the first few luxuries we buy. In my opinion, there’s some gray space between comfort, luxury, and what lies beyond luxury. Is a automatic coffee maker a comfort or a luxury? You could ask this question about lots of different items.

The point is: most of us have some guilty pleasures that do improve our lives. They are far from necessary, but they bring us happiness.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

The Slope Away from Optimal

Once you have some luxury in your life, the Fulfillment Curve argues that additional spending actually decreases your happiness. Having a working car is a comfort. Owning a Mercedes is a luxury. Owning a fleet of sports cars is a pain in the ass. That’s the simple idea.

“But I love cars, Jesse!” Fair enough…my simple example might not apply to you. But let’s imagine how the Fulfillment Curve might apply to food.

You spend a few dollars and buy a lot of rice, a lot of beans, bundles of bananas. Everything is cheap, calorie-dense, but a bit bland. Most important, thought, is that you won’t be going hungry. You’re surviving–that’s vital. But, it’ll get old pretty fast.

So we spend a bit more money. We buy some taco seasoning for our rice and beans. We add in some other fruits, some mixed greens, some pasta and sauce. This added flavor is a nice comfort to have!

We spend a bit more, and now we’re getting Oreos for dessert. Let’s bring back celebratory guest Notorious B.I.G., clearly a “luxury” grocery shopper:

So we can steam on the way to the telly, go fill my belly

A T-bone steak, cheese eggs and Welch’s grape

Well said, Biggie. It’s nice to get the occasional T-bone steak. And water gets old! Welch’s grape juice is a classic treat. And he adds cheese to his eggs? He really was a genius…

Going over the top

But then we continue to spend money on food. More and more money. We all know what happens next. The bananas go bad before we can eat them, and we throw some away. We grow fat on Oreos and T-bone steak and Coca-Cola. We realize that the grocery store is both gift and curse.

We’re spoiled for choice. We spend more money than we should on food that isn’t healthy, and end up throwing half of it away. Does this feel like optimal behavior?

Is it good to spend more than you need to? Is it good to buy things you know you’ll throw away? This is evidence that perhaps the Fulfillment Curve is onto something useful. Maybe there is an optimal point of spending, after which additional spending makes us feel worse.

The Fulfillment Curve in Your Life

You probably know somebody with more clothes than they could ever wear. They spend hundreds of dollars on clothes every year, only to give away a third of their wardrobe during every spring cleaning. Granted, the Fulfillment Curve is highly personal. For this clothes connoisseur, they might get lots of pleasure out of their spending. But for the average person, the headache and wasted money brought on by these over-the-top fashion finances is not worthwhile.

Another common occurrence: a garage so packed that it’s no longer used for storing cars. To each their own, but for me, this would be a sign that I’ve gone past the peak in the Fulfillment Curve. My possessions are starting to be a nuisance, preventing me from using my house as it was intended.

Speaking of which–storage units. Gee whiz. I’m not sure if all my international readers will know what I’m talking about here. But in America–and probably some other countries–some people have so much stuff that they rent out space on another person’s property to store that excess junk.

Let’s break this down for a minute. Our storage unit user deliberately separates their stuff into two groups. Group 1 is “things important enough to keep at home.” But Group 2 is “stuff so crappy that I don’t need it in my house.” And rather than getting rid of Group 2 (or preferably, not buying it in the first place), these people choose to spend more money just to store that junk somewhere else. They spent money up front, didn’t use the Group 2 items enough, and now are spending money to keep those items around anyway.

Yes, I’m being judgmental

Mea culpa. I know it’s not ideal. But I hope I’m giving you a slightly different lens to view this behavior–a behavior that many people would describe as “normal.”

It reminds me of another catchy phrase I saw recently (not from Notorious B.I.G., though):

Look around you.

That clutter used to be money.

And that money used to be time.

People are trading away more and more of their time and are slipping further down their Fulfillment Curves. It might be “normal,” but that doesn’t make it good. I, for one, am going to call on Biggie one more time: “I ain’t gonna keep puttin’ up wit the bulls***.” Word up.

The Benefits of Knowing Yourself

I think that self-awareness is a constant struggle, but very worthwhile. The better we know ourselves, the more successful we can be in all facets of life. If you know what the peak of your Fulfillment Curve looks like, you’ll find more success and happiness in your life.

So if you’re looking to walk away with some actionable advice today, keep reading.

Category by Category

Perhaps you maintain a budget in your life using some sort of category system. Money for Housing, Food, Entertainment, Travel…a wide assortment of categories to plan and then track your spending.

One benefit of my personal budgeting system is that I know exactly what I spend on each of these categories every month. So I can look at the $197 I spent on Dining Out in September and ask myself, “Was that survival? Was it comfort? Luxury? Or was it just excess?”

Alternatively, I can ask myself, “What’s my optimal level of spending in that category?” Ideally, I want to try out new cuisine. I want to treat my loved ones to a nice meal. But I enjoy cooking at home, and I know it’s more economical. So there’s a sweet spot–maybe 2-3 meals out per month–where I’ll feel comfortable and even luxurious, but don’t feel like I’m being overly opulent.

The Bigger Picture

Rather than breaking things down on a category level, a simpler method would involve looking at the big picture.

How much do you spend per month, and which spending feels wasteful to you? What items do you find yourself throwing away, and could those purchases have been prevented in the first place? What stuff is simply collecting dust? What’s just sitting there in the way as your maneuver around your house? If you needed a storage unit, what items would be the first to go there?

These are the kinds of questions that you can ask yourself to start chipping away at inefficiencies in your Fulfillment Curve.

Politics and Fulfillment

I don’t always dabble into political ideas here, but something about today’s topic is extremely poignant. Granted, I’m writing from the American self-centered point-of-view, but I bet this idea could apply in a few other societies on Earth.

America has millions and millions of people struggling to get to the simple survival point. Housing is expensive, medical care is obscene. In other words–there’s a significant poverty problem. These are matters of life and death.

Meanwhile, others are so skewed right on the Fulfillment Curve that they’re miserable. They spend and spend and spend, and are cursed like King Midas by their golden surroundings. When someone consumes to their own detriment, we usually call it addiction. How are the excesses of wealth any different than this?

My point is that we have large swaths of the population on either side of the Fulfillment peak. The solution is obvious. Both segments would benefit by moving towards the center. Tax the rich, feed the poor.

Santa Claus is coming…

‘Tis the season! So when you’re planning gifts for Little Tim and Uncle Ebenezer, consider the Fulfillment Curve.

What’s going to bring someone the most happiness? Probably something that takes them from survival to comfort. After that, something that moves them from comfort to luxury. But if someone already had everything they need, do you need to buy them something more?

It’s a very personal choice, I know. Sharing freely is a wonderful feeling. I don’t want to Grinch away your Christmas from you.

But I think it’s worthwhile to consider how your gift giving can best benefit the people in your life.

Feeling fulfilled?

The Fulfillment Curve provides a phenomenal change in perspective for the typical consumer. It teaches us to limit “more is better” thinking. It shows us that waste is more than a neutral behavior, but is actually a negative behavior. If we identify where we fall on the Fulfillment Curve, we can start to make meaningful changes in our lives that optimize more than our personal finance, but our overall quality of life.

Someone on the right side of the curve could wholeheartedly believe that “money doesn’t buy happiness.” But clearly, someone on the left side of the curve could name a hundred examples of how that’s simply not true. They’re both right. It’s all a matter of personal perspective.

So, tell me: how you do fit onto the Fulfillment Curve?

Thank you for reading! If you enjoyed this article, join 8000+ subscribers who read my 2-minute weekly email, where I send you links to the smartest financial content I find online every week.

-Jesse

Want to learn more about The Best Interest’s back story? Read here.

Looking for a great personal finance book, podcast, or other recommendation? Check out my favorites.

Was this post worth sharing? Click the buttons below to share!

Pingback: Andrew Carnegie's Cogs and the Path to FIRE ⋆ Camp FIRE Finance

Yes, yes, yes! This thought process is precisely what I go through when planning big purchases like travel. The peak of the fulfillment curve for our family is a hotel with free breakfast and a pool. Paying more than what those hotels charge often puts us into a business-class hotel that doesn’t offer free breakfast and does not cater towards kids. Spending more on hotels then decreases our happiness!

Hey Kim, thanks for the message! That’s such a good example. I can certainly remember, as a kid, only caring about the pool! “What more would anyone ever want?!”

P.S. I just checked out your blog. First, I’d love to guest post if you’re interested. And second, you live in Wyoming?! My girlfriend is from Jackson, and we went back for a visit there this past August. It was amazing!

Hey Jesse! Let’s connect thru email & go from there, I’m happy to have found you and your blog!

Pingback: What's Up Wednesday - Volume 13 - The Frugal Engineers

Pingback: Travel is Overrated - How We Save on Travel - The Frugal Engineers

Pingback: Net Worth Targets by Age - The Best Interest - 25th, 50th, 75th percentiles

Pingback: Semi-Retirement Savings Rates - How Much Do You Need to Save? - Semi-Retire Plan

Pingback: How to Balance Saving for FIRE & Enjoying Today - The Frugal Engineers

Pingback: What's Next? - The Best Interest - Future steps, one day at a time

Pingback: Living On Less: The Average Cost of Living vs. Average Wages - My Life, I Guess

Pingback: How to Put the "Personal" in Personal Finance - Money Saved Is Money Earned

Pingback: The 45 Top Personal Finance Blogs ( And Why You Should Read Them) | Money Week

Pingback: The 45 Top Personal Finance Blogs of 2020 (And Why You Should Read Them) – Finance Market House

Pingback: The 45 Top Personal Finance Blogs of 2020 (And Why You Should Read Them) – The Providence Times

Pingback: The 45 Top Personal Finance Blogs of 2020 (And Why You Should Read Them) | Market World

Pingback: The 45 Top Personal Finance Blogs of 2020 (And Why You Should Read Them) | Share Market Pro

Pingback: The 45 Top Personal Finance Blogs of 2020 (Why You Should Read Them) - HealthyLifey

Pingback: The 45 Top Personal Finance Blogs of 2020 (Why You Should Read Them) – Credit News

Pingback: The Best Leadership Quotes and How to Apply Them - Debt-Free Doctor