I am not a money genius. I’ve touched many proverbial “hot stoves,” and the Best Interest is part of my scar tissue. Today, let’s dive into seven of my money mistakes and the lessons I’ve learned from them.

Money Mistake #1: Not “Renting My Fun”

I once heard radio host Colin Cowherd say, “Buy ‘normal life,’ but rent your fun.”

It makes sense to buy healthy groceries. It makes sense to buy comfortable shoes. It makes sense to buy a reliable car. You need those things every day of your life.

Life is a constant.

But fun might be seasonal or weekend-only. Does it make sense to buy a snowmobile that you’ll only use eight weekends a year? Maybe. It might fall high on your bimodal passion graph.

Does it make sense to buy a boat? I have coworkers who sail every weekend during the summer. They plan sailing vacations on Lake Ontario. They love sailing. A full purchase makes sense for them.

But for the rest of us, renting a boat or snowmobile makes better financial sense. It’s too easy to overspend on a shiny object you’ll underuse

I’ve discovered a second category of “fun objects”: those that are fun only due to confounding factors.

Is a hot tub fun? Or is a hot tub fun when you’re hot tubbing with other people? That’s the lesson I learned…and the money mistake I made because of it. It’s a story I’ve written about before here on the Best Interest.

I bought a hot tub. It’s great, especially on cold winter nights. But my rationale for buying the hot tub was, “Hot tubs are great!”

We checked the record, and that rationale was determined to be false.

Hot tubs aren’t great. Hanging out with other people in a hot tub is great. Oops.

I could scratch my hot tub itch with a few trips per year. The rest of the time, I should just try to hang out with my friends more often. Thankfully, I didn’t use credit to buy the hot tub. I didn’t borrow money for it.

But it was an impulsive purchase. It didn’t mesh with my financial goals. The hot tub is nice, but buying my fun (rather than renting it) was a money mistake.

Money Mistake #2: Decrease Spending vs. Increase Income?

In this world of credit card debt and budgets and dwindling emergency funds, it makes sense to spend less. That’s the easiest way to save money. We can enact it today. Just spend less!

But is it the most consequential improvement? I say no.

Over the long term, you’ll be much better off making efforts to increase your income. Why? Let’s do some quick math.

Sadie makes $50,000 per year. Of that, she saves $10K. The other $40K goes towards bills—that’s $3300 per month.

If Sadie needed $500 extra this month, she could cut her $3300 monthly budget down to $2800. Scrimp and save.

If Sadie needed an extra $1000 this month, she might be able to cut that $2800 monthly budget down to $2300. Do you see where this is headed?

At some point, Sadie can’t cut any more fat from her budget. She’s limited by her survival needs. Frugality and cost-cutting have lower limits. They are bounded.

But increasing your income, technically speaking, is unbounded. The upper limit does not exist.

In reality, we’re not all going to be billionaires. We will eventually hit an income ceiling.

But Sadie can make a plan to increase her salary. She can look for promotions within her company. She might be able to switch jobs and leverage a raise that way. Making more money is possible for many people in many professions.

For my first few years of personal finance stove-touching, I focused on reducing expenses. And it worked! But I eventually hit a lower limit.

Then I looked for ways to increase my income. The results were fast and fantastic. I found a new job, negotiated my salary higher than offered, and secured the easiest 30% raise of my life.

Cutting spending is fine. Start there, it’s ok. But it’s a money mistake to neglect ways to increase your income.

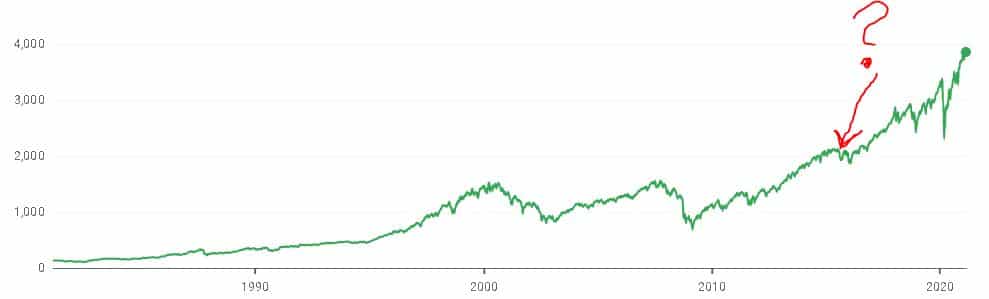

Money Mistake #3: Listening to Mr. Market

I read a lot of information about personal finance and investing. I’ve done so for years. And there has always been someone calling for a crash, a burst bubble, or a bear market.

See—here’s an example from 2015. Meanwhile, how has the stock market actually performed since 2015?

We’re risk-averse, over-developed monkeys. Fear is normal. But we should try to delineate between irrational reactions to fear and rational reactions to facts.

Ben Graham’s famous Mr. Market parable personifies this irrational fear. If you’re not familiar with Mr. Market, follow that link and read up.

When I was new to investing, I listened to Mr. Market. And that was a money mistake! I let my investing choices be controlled by irrational fears.

As a result, I didn’t max out my investing accounts (which I’ve changed now). I estimate that I under-invested by about $20,000 in 2014 and 2015. It’s an opportunity that I’ll never get back.

Fast forward to today, that $20,000 mistake is worth about $40,000. Keep going to 2040, and that mistake is likely to surpass $100,000 in value.

There’s no use crying over spilled milk. It doesn’t keep me up at night. I’ve learned my lesson, and I won’t make that mistake again. And I hope you learn from my money mistake too.

P.S.—if you’re worried about an impending market crash, I 100% empathize. I get it. I recommend you read this and let me know if that helps.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Money Mistake #4: Caring About the Joneses

We’ve all heard it before. “Keeping up with the Joneses.” Buying nice things simply because your peers—the Joneses—have those nice things.

But as I pointed out on the Rochester Business Connections podcast:

“The Joneses might be broke.”

-Jesse

It’s easy to forget that fact. The Joneses might be stretching—and stressing—their budget to a near-breaking point. Are you sure you want to keep up with that?

I worked at a software company after university. They hired tons of 22-year olds like me. And I immediately noticed that many of my peers had nice stuff.

They drove $50,000 cars. They wined-and-dined most nights. They planned cross-country trips on a whim—what’s a round-trip flight, $1000? Chump change.

I know that pang of envy. I wanted those things too! How were my peers—ostensibly on a similar salary as me—living these lavish lives? There are two obvious answers:

- They had different budgets and different priorities.

- They had alternate sources of income.

#1 makes will always be true. Everywhere you look in life, people will spend differently than you. My coworkers made conscious choices to spend on nice items. I put my money to different uses. That’s neither good nor bad. It’s just different. Each person spends differently.

And #2 is something I have zero control over. Some people are born on third base. Others are born in the ditch. It’s not fair. It’s just luck. I enjoy writing about the role of luck in society.

(But I certainly shouldn’t feel bad that some people are luckier than me. I’m very lucky in my own life.)

Once I’d convinced myself of these truths, my money mistake became obvious. Let the Joneses do their own thing. They’re on their own path. I have my path.

Money Mistake #5: Hunting Mice, Not Gazelles

Why don’t lions hunt mice? What chance does Mickey have against the lion king? Lions could hunt mice in spades!

But the energy gained from that small mouse isn’t worth the lion’s effort. The lion is better off hunting gazelles.

We can—and should—apply a similar thought process in our lives. It applies to time management. It makes sense at work. And yes, it makes sense in personal finance.

Don’t hunt the field mice in your money life. It’s a common money mistake. My favorite example is this classic:

“I’ll drive across town to fill up my gas tank…gas is 20 cents cheaper at that gas station!”

This is quintessential mouse-hunting. Driving 5 miles (which has a cost) over 10 minutes (what’s your time worth?) in order to save, let’s say, 20 cents/gallon * 15 gallons = three dollars!

You are spending—both in time and money—more than you’re saving.

I’m not saying, “Don’t go after free money.” I would certainly pick up three dollars if it was lying on the sidewalk. That’s because sidewalk money costs me two seconds of time and one solid bend of my back.

But this gas savings had a real cost. That cost completely negates the benefit. The $3 gas savings is not free! To ignore that fact is a money mistake.

It’s the same reason lions don’t hunt mice. Some “easy prey” simply aren’t worth the effort.

Money Mistake #6: Servant or Master?

Various philosophers are attributed with saying:

Money is a great servant but a bad master.

This is certainly a lesson I’ve learned the hard way, and continue to learn—both through normal life and through my blog & podcast projects.

Money is nothing but a tool. Nothing more, nothing less. Tools help us build. But you probably know some people who classify as ‘tools’—and you don’t want them to be your master!

Jokes aside, there’s a slippery slope towards letting money control you. I’m pretty transparent here on the Best Interest. I’m in a healthy money situation and have been for a few years. But I still stress periodically. Without fail, that stress is due to my letting money become more master than a tool.

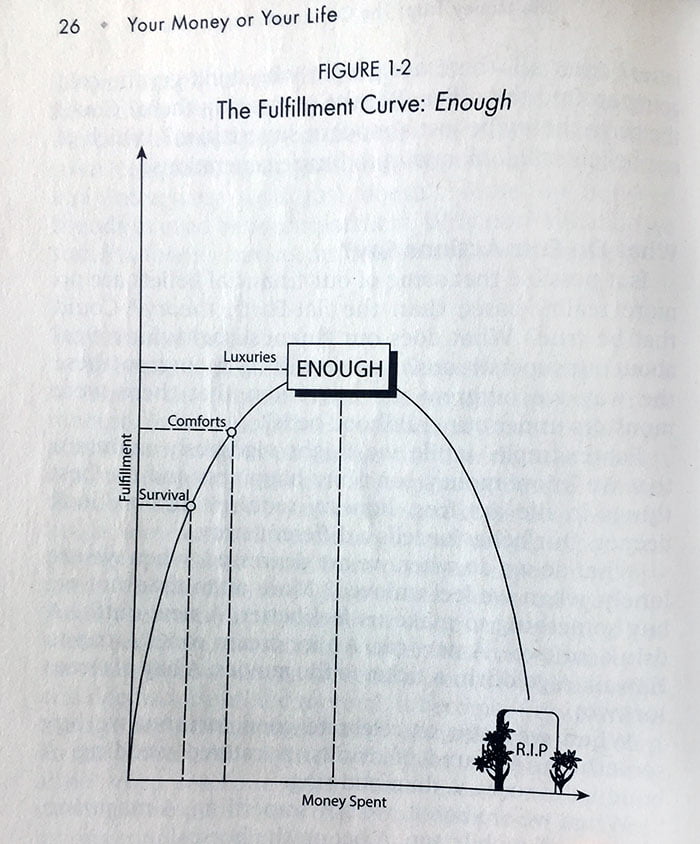

Perhaps my favorite articles to write are the ones that involve the psychology of money. Stuff like the fulfillment curve and the aforementioned “bimodal spending.”

There’s a pattern in my articles. That same pattern is borne out when other financial writers discuss the psychology of money. Namely, we all ask: how do we optimize money as a tool and minimize its role as a master.

Money Mistake #7: No Budget, No Clue

For many years, I operated without a budget. It’s true.

Yes, now I’m a budgeting fiend. But there was a time when I had zero clue where my money was going. And that, no surprise, was a massive money mistake.

I’d check my bank accounts occasionally. I knew—roughly—what I spent on groceries and gasoline. But I couldn’t tell you for sure. And I certainly couldn’t have found any good ways to improve my finances.

It’s funny. Because of my lack of knowledge, I can’t even tell you the opportunities that I missed! That’s scary in-and-of-itself. As I wrote in the “Budget Basics” article, all of the experts I spoke with budgeted. They all monitor their spending in some way.

Readers, you don’t have to be a zealot like me. As I outlined in my 2019 review and 2020 review, I budget like a maniac.

But you can’t just “do nothing” when it comes to budgeting.

No More Money Mistakes?

No, no. I’m sure I’ve made tons of other money mistakes. But we’ll stick with those seven today. Quick recap, they were:

- Not “Renting My Fun”

- Decrease Spending vs. Increase Income

- Listening to Mr. Market

- Caring About the Joneses

- Hunting Mice Instead of Gazelles

- Letting Money Be My Master (Instead of Servant)

- No Budget = No Clue

Feel free to chime in with some of your money mistakes below. It’s ok. We’ve all messed up before 🙂

Thank you for reading! If you enjoyed this article, join 8000+ subscribers who read my 2-minute weekly email, where I send you links to the smartest financial content I find online every week.

-Jesse

Want to learn more about The Best Interest’s back story? Read here.

Looking for a great personal finance book, podcast, or other recommendation? Check out my favorites.

Was this post worth sharing? Click the buttons below to share!

This post is my favorite so far. Congrats on the Motley Fool recognition! Well earned.

Thanks Craig!

Nice article to understand

Thanks Jazaa!